Published 8/11/24

Deutsche Beteiligungs AG(DBAN) – Middle Market PE Firm in Germany

Deutsche Beteiligungs or DBAN is a small German based middle market private equity firm that currently manages 2.5B in AUM. The company is valued below book value which assigns no value to its investment fee income which makes it attractively valued. Peers usually trade at a premium to book and 10 to 20 times fee related income. The company has recently expanded to Italy and into private debt which will allow the company to continue to grow AUM. I think DBAN is probably a nice place to park my money for the future.

Macro

I’ve been bullish on private equity for a while, investing in Onex corp back in April 2022(which has been about flat since) and also investing in Vinci(also about flat) in 2023. Deutsche Beteiligungs will be my third investment in the sector. The reason I’m bullish private equity and also private assets is due to the structural tailwinds that are pushing more assets into the asset class. This is summarized by three main points

- Lower volatility due to not having publicly traded portfolios which LP’s and asset allocators greatly desire

- Higher returns than public markets historical(using leverage but nobody adjusts for that)

- Higher costs and increasing regulations of public markets(the number of public market companies in the US has declined dramatically since sarbanes oxley.

Barring all these continuing I see no stopping total private AUM from increasing into the future. With most estimates putting AUM growth between 5–15% for the next decade.

Also private markets are quite fragmented with the Private Equity industry having over 11,000 firms. The top 25 players only control 2% of AUM. Private credit, the largest of the alternate asset markets, is much more concentrated with 10% of AUM owned by the top 5 players. This means firms can grow faster than the market through consolidation which is what Deutsche Beteiligungs AG recently did with the acquisition of Elf Capital in 2023.

Additional DBAN is quite small with only 2.5B in AUM which is the smallest publicly listed asset manager that I have found. If you believe like I do that the bigger a asset manager becomes the harder it becomes to outperform than DBAN size will be an advantage for years to come as the Apollos, Blackstones and KKR’s begin to choke on their own size as they eclipse $1 Trillion in AUM each, which will help the smaller players in the space.

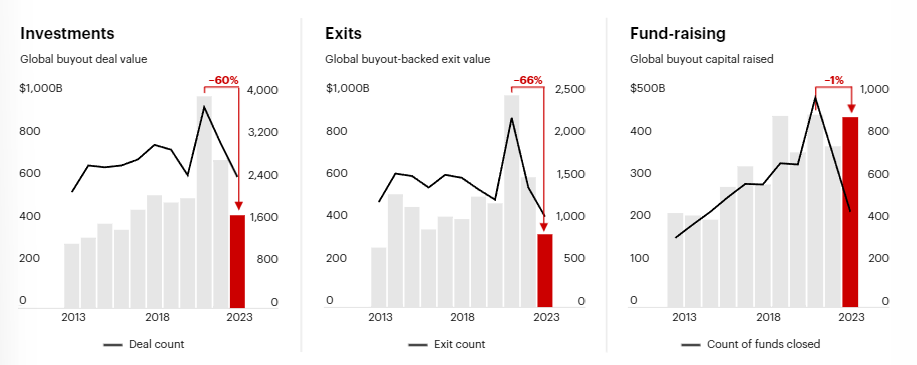

Recently private markets have taken a turn as deal value and count have fallen nearly 60% from 2021 and back to depressed 2020 levels. Which is due to the rapid rise in interest rates and fall in exit multiples. I think this is short term as the market will eventually adjust to the new conditions or interest rates with finally start to follow inflation down.

Source: Bain 2024 PE Outlook

Overview

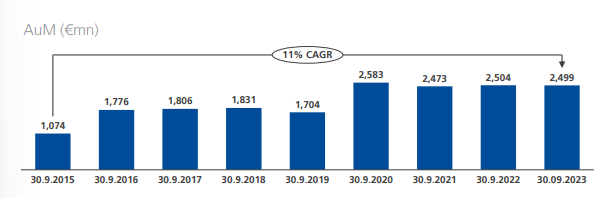

Deutsche Beteiligungs AG has been around since 1965 and was focused exclusively in middle market private equity in german speaking countries such as Germany, Austria and Switzerland. In 2020 the company began investing into Italy, opening up more opportunities for the company. In addition to this in 2023 the company acquired a majority stake in ELF Capital which is focused on the Private Debt markets. Private debt is much larger than private equity so AUM could be growing much faster growing forward. In aggregate DBAN has grown AUM from 1.1B in 2015 to 2.5B as of the end of 2023 which is a 11% CAGR.

Source: 2023 DBAN Presentation

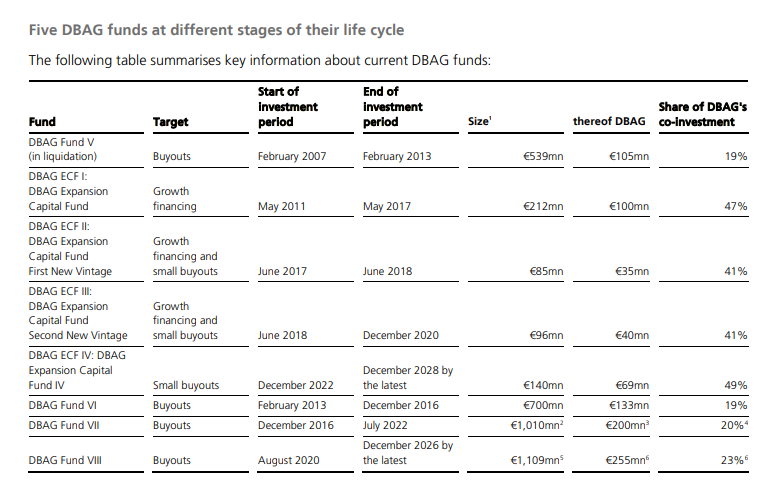

DBAN’s main fund is simply named DBAN Fund is in its eighth iteration. Each successive fund has gotten bigger with DBAN V in 2007 being 500M and DBAN VIII being 1.1B in 2020. DBAN VIII though was only slightly bigger than DBAN VII though I think that was because fundraising was during 2020. Each main fund has been raised around 3-6 years after the prior fund. Since DBAN VIII was raised in 2020 DBAN VIIII will most likely be raised either in 2025 or 2026.

Source: 2023 DBAN Annual Report

Looking at performance of DBANS funds which is the best indicator of future AUM growth, DBAN is inline with peers at a 2.5X MOIC or Multiple on Invested Capital. A 2.5x MOIC is inline with peers that I looked at such as KKR, Carlye, Bridgepoint, and Tikehau. Now fund performance and AUM growth might be inline with peers but DBANS valuation is certainly not.

Source: 2023 DBAN Presentation

Valuation

DBAN is currently trading below book at a .7 P/B Ratio. When valuing a private asset manager you usually separate its invested capital and its asset management fee business and value each separately. Because the invested capital is invested in the funds that the company manages and grows or declines based on the performance of the funds usually growing around 10-15% justifying a value of 1 to 1.5 times book.

The asset management business grows not based on the capital of the business but through client funds though it is somewhat correlated as the private asset manager must put some money in its own funds though as the manager gets bigger usually the proportion of the managers funds to client funds declines. The management business earns a fee on the amount of client funds it manages and so as long as performance of those funds is looking good the earnings from that is pretty sticky justifying a multiple on fee earnings of 10-20 times. You then add the value of the invested capital to the fee earnings multiple to get the value of the business. There is also performance fee income if the manager gets client fund performance above a threshold but I’ll just treat that as extra juice to squeeze.

Looking at other smaller european listed peers such as Bridgepoint and Tikehau Capital both with about 40B in AUM trade at over 1 times book and 10 times Fee earnings.

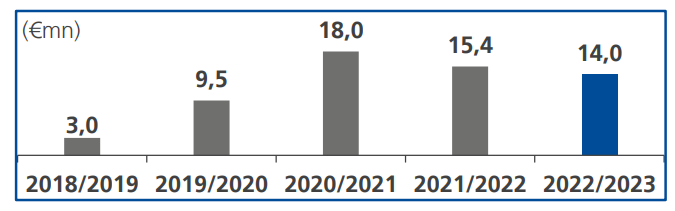

DBAN isn’t only a book value play as the company also has a bit of fee earnings from its asset management side. Income from fund services has increased alongside the companies AUM as from 2015 to 2023 income from fund services went from 18M to 46M.

Source: 2023 DBAN Presentation

I think this also includes performance income as earnings from fund services is quite volatile. With a minimum income of 3M and max of 18M within the last 5 years which averages 12M.

Source: 2023 DBAN Presentation

Adding current NAV to a 10 times multiple to fund earnings would give you a valuation of 788M. Considering the current market cap as of today’s date was 482M I would say the company is quite undervalued.

Source: 2023 DBAN Presentation

Insiders

Rossmann Beteiligungs GMBH is the largest shareholder with a 25% stake which was achieved in 2019 so that implies they bought shares to get their stake. Looking at the annual report it looks like the company was controlled by this company pre 2013 as there was an agreement in 2013 for Rossmann Beteiligungs to relinquish control from DBAN. So this implies that Rossmann Beteiligungs is the founder’s holding company.

Besides that, looking at share purchases management has been buying stock recently. Also I like management comp as they are paid based on NAV and income from fund services growth. 8% hurdle rate on NAV growth.

Risks

Continuation of Poor PE Market

Due to higher rates the private equity market as been depressed if this continues it may affect the companies ability to raise funds and thus increase revenue.

Poor Fund Performance

The goal of an asset manager is to collect more assets to charge fees to. If the performance of the asset manager’s fund dips too low clients may pull money out instead of put money in. The performance of DBANS funds will be key to watch.

Summary

I could try to project some expected return for DBAN but it seems cheap enough to where that doesn’t seem necessary to me. The company has grown AUM since 2015 at 11% which assuming the private markets get back to normal in the next 5 years I think DBAN can grow much faster than that with them entering into Italy and getting into private debt which is the largest of the private markets and the big PE players like Apollo, Blackstone, and Ares all got that big mostly through private debt.

Top four metrics

To make it easier to track my investments, I’ve been finding four metrics for all my investments. For DBAN I will track the following to give me jest of their performance for the years ahead.

- NAV

- AUM Growth

- Earnings from Fund Management

- Fund Performance