Published 11/3/22

ACEA SPA: Largest Italian Water Company Trading at a 6% Div

Introduction:

Founded in 1909, ACEA is a multi-utility operator. ACEA is the largest water utility in Italy also operating in Latin America. ACEA’s other segments include energy, engineering, gas, and waste management. European stocks have been getting killed this past year as Russia invaded Ukraine and has created an energy crisis throughout the continent. Italy in particular was adversely affected. This situation has created a great opportunity within European stocks, especially with a company like ACEA which is in one of the safest businesses of all time, a water utility. ACEA is trading at a 6% dividend yield and a 9 PE Ratio. This is a massive undervaluation compared to peers in the US and UK. The company is mostly facing macro issues but the future is probably brighter than the current stock price suggests.

Macro

In the Macro section, I’ll look at the three big picture things affecting the stock which include the European situation, the Euro which as a US investor affects my return, and the water industry in Italy which is where problems and opportunities collide.

Europe

Stocks globally have been in a bear market this year due to slowing economic growth and recession. Because of the Russian invasion and energy crisis, Europe in particular has been hard hit.

Italy measured by ticker EWI is down 28% and Germany’s ticker EWG is down 34%. While Spain(EWP), France,(EWQ), and the US(SPY) have held up much better. The downturn in European equities has created an opportunity to find undervalued companies.

Euro

The euro has also been in a downturn this year against the US dollar. This decline can be attributed to the ECB’s weak response to inflation, the Russian invasion, and the European energy crisis.

The weakness in the euro has not translated to an undervalued currency yet. According to the Big Mac index the euro is trading at a 4% premium compared to the US dollar on a GDP-adjusted basis. Considering the Big Mac Index isn’t super precise the currency should be considered fairly valued. Over the long term, the EU is a current account surplus nation which is a positive for the Euro longer term. Short term however because of the energy crisis, the EU has seen a negative trade balance which is a negative for the currency.

European Balance of Trade Chart

The main drag on the currency is the supply and price of energy in the short term. A bet on the euro is a bet that things normalize. Already we’re seeing a much warmer winter which will decrease demand for nat gas and if more supply can come from America the energy crisis could be solved or at least not as bad. Nat gas prices have come down from their highs in August 2022 from €340 to €112 at current prices. This is still much higher than pre covid prices of around €40.

In the short term, there may be continued pressure on the Euro depending on how the energy crisis plays out in Europe. Historically the Euro has traded at a premium to the dollar so there is the potential longer term for the currency to add some return to the investment. For the most part, however, I expect the Euro not to affect the performance of an Investment into ACEA much, as according to the Big Mac index it’s about fairly valued.

Italian Water Utility Industry

ACEA largest segment by EBITDA contribution is water which contributes over half of the company’s EBITDA. So that is the sector I’ll look at from a Marco perspective. Water is also a sector management continues to look to grow.

The Italian water utility industry can be categorized by low prices, horrible water efficiency, decaying infrastructure, and mostly government-owned.

In the beginning, most utilities in Italy were set up by local city governments. This ownership still continues to this day as most water utilities in Italy are either fully public or only partially privatized. In total 54% of the market is serviced by fully government-owned players. Another 42% of the market is serviced by mixed shareholders with both public and private interests. ACEA is an example of a mixed-class company as the company is majority owned by the city of Rome. with the other 49% of the company privately owned. The remaining 4% of the market is serviced by fully privatized players.

Government players have been the source of poor service quality and below average prices. Italy has some of the worst water efficiency in the world with 41%(2021 ARERA Annual Report) of the water pumped getting lost in the pipes and not getting to the end user. This compares with Germany which only has 4% of water lost in transit to end users. This water efficiency problem is caused by a lack of investment in infrastructure in the previous decades. Investment fell from 2B to 600M over the 1990’s into the 2000’s. This is because politicians don’t want to raise prices as raising prices can be a sensitive issue during elections. However, unless prices rise there is no incentive for investment. Investment has come back however in the most recent decade but prices still remain very low. Water in Italy averages around €2 a cubic meter while in France the average is twice that at €4.

The lack of investment also has hurt water quality. In Italy according to ISTAT 2021 report close to 30% of the nation’s households don’t trust the nation’s tap water. To solve these problems the Italian government has kept pushing for much more consolidation and privatization of the industry. They have done this through legislation like ATO’s which are meant to create single operators for a given region in Italy, also the Galli Law and a 2010 privatization referendum.

The Italian Water Utility industry is a €7.8B market according to the 2022 Blue Book. ACEA with €1.2B in revenue in 2021 is the largest player with 15% market share. This brings an advantage of profitability because of the company’s scale. The company enjoys 50% EBITDA margins compared to the sector average of 37%(Data from 2022 Blue Book). The Industry isn’t that consolidated, however. The biggest 16 companies that have revenue of over €100M control 53% of the market.

There are 25 companies with revenue between €50-€100M, 24 companies with revenue between €25- €50M, and 166 companies with revenue below 25M.

The industry’s problems and fragmented nature create an opportunity for ACEA. With increased full or partial privatizations from a fragmented industry, there will be plenty of opportunities for ACEA to acquire other water utilities in Italy. The smaller players also have much lower profitability due to being subscale which means ACEA could potentially be able to pay a higher purchase price than other players giving them an advantage when it comes to consolidation. ACEA water efficiency is much better than the Italian average for example, in Rome ACEA’s water loss is only 28% as of 2021. This gives another reason why ACEA could be the preferred acquirer. The low water prices across Italy also present another opportunity because if they come up to the European average this would benefit ACEA greatly. Other sectors that ACEA plays in have similar characteristics as water does.

Financials

ACEA’s financial performance as measured by ROE has been quite strong especially compared to peers. This has been done with about sector average debt metrics.

Roe

The most important metric for a utility is its ROE or return on equity. As an asset-heavy industry, ROE measures the efficiency of the capital used in the business. It also measures management competence in investing capital.

ACEA’s(Ticker: ACE) ROE is one of the best in the sector. I measured ROE by averaging the last three years. ACEA came out with an ROE of 14% vs a sector average of 9%.

Debt

ROE can be skewed by a lot of debt. So I compare ACEA’s debt load to peers to see if debt is propelling their ROE. I look at debt/equity and operating cash flow/interest expense ratio.

In terms of ACEA’s debt/equity ratio or D/E, it is about average for the sector. ACEA D/E Ratio is 3.2 vs the sector average of 2.8. This means that ACEA’s superb ROE is not just because of a larger debt load.

In terms of operating cash flow/interest expense or OCF/I ACEA comes out much better than the sector average. For this metric the bigger the better. ACEA’s OCF/I is at 7 compared to the sector average of 4.2. This is due to higher OCF margins and lower weighted average cost of interest.

One negative about the debt that ACEA carries is the average duration. ACEA’s average debt duration is 5 years. Peers such as Severn Trent(Ticker: SVT) and Artesian Resources (Ticker:ARTNA) have average durations over 10 years. ACEA’S weighted average cost of interest is 1.8%, if the current interest rate environment continues for the next five years the company would have to roll over the debt at much higher rates, eating into profits. So that might be a reason why the stock trades at a lower valuation than peers.

Growth

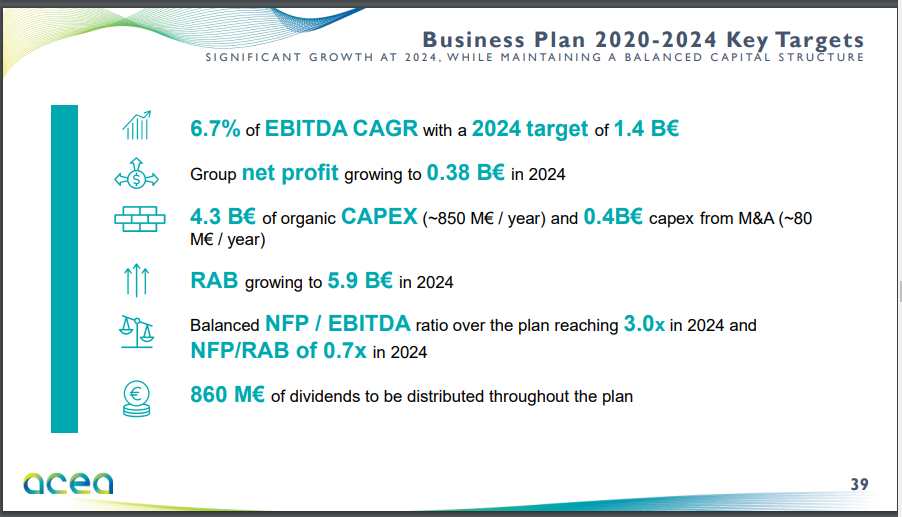

ACEA has grown Revenue at a 7% CAGR since 2016 and earnings at 5% CAGR. ACEA is projecting 6.7% EBITDA growth CAGr through 2024. This projection is from ACEA’s recent 2020-2024 business plan. ACEA previous two business plan projections such as their 2016-2020 and 2019-2022 were both achieved. The achievement of both EBITDA targets from the previous business plans shows management’s ability to execute and the stability of the industry.

Source: ACEA 2020-2024 Business Plan Presentation

ACEA’s Fastest growing segments include their environment segment which is basically waste management, engineering & services, energy generation, and overseas water segments. These segments are still quite small compared to Water.

For the most part, the company’s strategy for growth is to continue to acquire and consolidate in the sectors they operate in. As explained above the water sector in Italy is still very fragmented and there is plenty of opportunity to continue to consolidate. The other sectors where ACEA plays in, also have similar dynamics to the water sector and should prove to be ripe grounds for acquisitions.

Insiders

ACEA’s main owner is the city of Rome with 51% ownership, and the second is Suez Environmental with 23% Ownership. Suez is merging with Veolia Environmental sometime this year. Veolia Environmental is the largest water utility in France and I think in the world. 5% of the company is owned by the Caltagirone family. And finally, the rest of the company is free float.

Executive Comp

- There is a Fixed component, with short-term and long-term components.

- The fixed component is the largest one

- The short-term component averages 47% of the Fixed component

- The long-term component averages 30-50% of the Fixed component

- KPI’s for short-term comp

- NFP (weight 30%);

- EBITDA (weight 30%);

- Net Profit (weight 30%);

- Composite Sustainability Objective (weight 10%)

- KPI’s for Long Term (IE 3 year Period)

- Cumulative EPS (weight 40%);

- NFP/EBITDA (weight 25%);

- NFP/Net Profit (weight 25%);

- Composite Sustainability Objective (weight 10%).

- NFP= Net Financial Position or target Debt

- Summary

- Executive comp is adequate

- EPS targets earnings growth net dilution

- NFP makes sure they don’t go overboard with debt

- Numerous profitability measures to ensure profits are prioritized

- Not sure about EBITDA though.

- (LINK)

Risks

The main risks for the investment I see are interest rates, Water Contracts, and a declining population.

Interest Rates

As mentioned above ACEA’s average loan maturity is 5 years and the cost of debt is 1.8%. Current short-term rates in the US are above 4%. If the current Interest rate environment were to last for another 5 years refinancing at rates 2-3 times higher would be likely. This would eat profits significantly. However, looking at most price charts like housing, nat gas, and steel leads me to believe deflation and thus lower rates are on the horizon.

Water Contracts

ACEA signs long-term agreements to manage the water cycle for the various municipalities they operate in. Technically at the end of the agreements, the province could tender the contract to another operator. ACEA signed a few contracts in the early 2000s that expire in the 2030s. If ACEA can’t convince the city to renew this could result in large losses to revenue. There is no indication currently that this would happen.

Declining Population

Italy’s population is projected to decline from about 60m in 2022 to around 48m by 2070. This decline in population will probably coincide with a decline in water, waste, and electric volumes. This obviously will be bad for ACEA in the long run.

However, in the medium term around the next 10-15 years, ACEA should continue to grow for two reasons. One is the industries the company plays in are set to consolidate for the foreseeable future. Second is that even though the population of the county has started to decline, urbanization is still continuing. That means that the large cities are still projected to grow in size into 2035. For example, Rome which has 4.3m people in 2022 is projected to grow to 4.5m in 2035. This is true for most of the large Italian cities. ACEA’s main businesses are located in large cities so in the medium term it will be shielded from volume declines. In fact according to worldometers even as the Italian population is projected to decline by 6 million by 2050 the urban population will grow by 2 million.

Valuation

ACEA trades at a significant discount to UK and US peers. They share this discount with their Italian peer, Gruppo Hera(Ticker:HER). The UK water utilities also trade at a large discount to their US peers but not as large as ACEA and Hera. So I can probably say that the European crisis is causing European water utilities to trade at a discount to American water utilities. Due to extra perceived vulnerability in Italy to the energy crisis, Italian stocks are trading even cheaper than UK stocks. ACEA(Ticker:ACE) trades at a 9PE and 6% dividend yield vs a peer average of 32PE and 3% dividend yield.

| Ticker | P/E | Div Yield |

| ACE | 8.7 | 6.09% |

| HER | 9.1 | 5.46% |

| SVT | 24.6 | 4.06% |

| AWK | 27.6 | 1.66% |

| ARTNA | 28.2 | 2.05% |

| CWT | 28.9 | 1.59% |

| Average | 31.9 | 2.95% |

| WTRG | 32.2 | 2.30% |

| YORW | 32.8 | 1.76% |

| AWR | 34.5 | 1.59% |

| CWCO | 38.5 | 1.85% |

| UU | 39.4 | 4.57% |

| SJW | 39.6 | 1.94% |

| MSEX | 40.3 | 1.25% |

Expected Return

Below I estimate the expected return based on my projections.

Expected 5YR CAGR

| Stock Price | €12.80 |

| 5YR Earnings CAGR | 6% |

| 5YR EPS | 1.96 |

| Earnings Multiple | 10 |

| Future Share Price | €20 |

| Div Yield | 6% |

| 5YR Expected Return | 15% |

Assumptions

I assume a 6% earnings growth which is slightly less than management’s EBITDA projections. Management has historically been quite accurate with their projections. Along with this, I assume a slight multiple expansion to a 10 PE. Because in 5 years things on the Marco side should clear up. The sector average is 32 and ACEA itself was trading at 15 times earnings before the Russian invasion so a 10 PE is quite conservative. If anything there’s a big possibility if things clear up in Europe that the multiple will be quite higher. With a projected share price of €20 in 5 years, that equals a 9% CAGR from current levels. Add the 6% dividend yield and that gets you to a 15% expected 5-year return.