AF Legal: Australia’s Legal Roll Up

Introduction

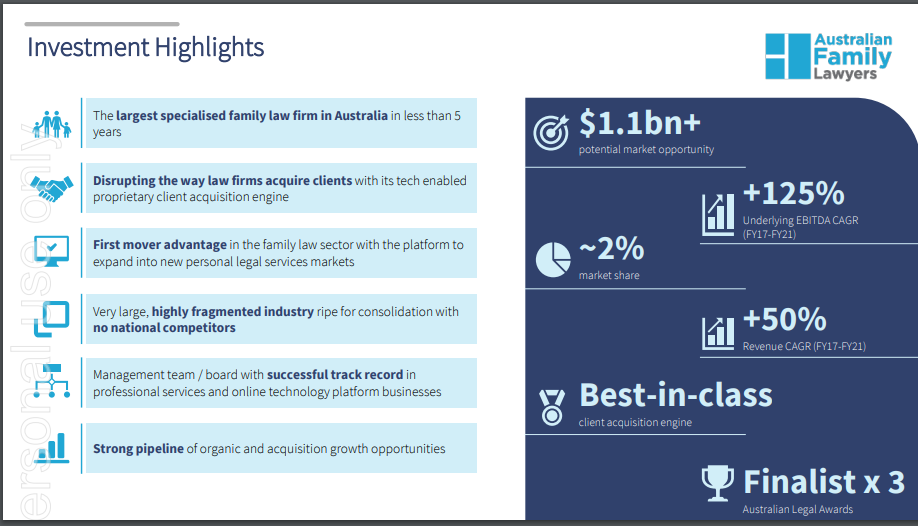

AF Legal is a law firm rolling up the family law market in Australia. Family law is a branch of law focused on divorce, separation, property and children matters. AF Legal is growing fast since listing revenue and ebitda CAGR are 50% and 125% with less than 2% market share in the family law market in Australia. AF Legal is able to acquire other family law firms at very attractive multiples of 1.5-3.5 times EBITDA or 3-7 times FCF. AF Legal also has great return on capital metrics clocking in over 20% ROIC as of H1 2022. The market opportunity is large for AF Legal and so AF Legal should be able to keep growing at this fast clip, acquiring companies at cheap multiples, and having great returns on capital.

Currency Blurb

As an Australian company the company transactions in the Australian dollar. According to Trading Economics the country as of Q4 2021 is experiencing a current account surplus. This is a positive for the currency in the short term.

This is most likely due to the higher commodity prices worldwide. This will likely only last for the short term. Another Bullish indicator for the currency is the Big Mac Index published by The Economist. As of Dec 2021 the Big Mac Index has the Australian Dollar as 16% undervalued against the dollar. I don’t see currency swings being a big driver of returns for this investment however it is nice to see that both of my favored indicators for currency fundamentals are pointing to appreciation.

Market Opportunity

As a law firm specializing in divorces the number of divorces would be an important indicator for the market size.

Peaking in 1976 the number of divorces has been declining ever since. This comes at a time when the amount of marriages were increasing. So from the data this seems to suggest that people either are loving more or are picking their partners better than the past. Also another reason could be the aging population. As you get older and the longer your marriage lasts the less likely divoce becomes. So as the population ages so too should the divoce rate decline. The declining rate and number of divorces is a positive for love but a negative for AF legal. This decline however has been quite gradual at a -1% CAGR.

Even though the volume of divorce is declining the dollar size of the market is very large and is probably still growing as the cost of divorce outpaces the volume declines. That outpacing is mostly my assumption as legal inflation has outpaced regular inflation since the 1980s. AF Legal is quite small with only 22 million in run rate revenue as of 2022 H1 report. AF Legal estimates the family law market to be 1.1B. Now I couldn’t independently verify this firgure however I found various data points to try to estimate it. The average cost of a divorce is very difficult to find. Combining through the internet I found a simple divorce to cost between 1000-3000 AUD. Adding any complexity to that like asset disputes or children could cost another 5-10K. And if you have to go to court that’s another 5K a day.

Chart: Moneymag

According to Moneymag, an Australian magazine a divorce that goes to trial could cost 82500-158000 AUD. With around 48000 divorces a year and 1.1B spent in legal fees this implies 23000 AUD for an average divorce. So I think that AF Legal’s estimate of their market size is reasonable.

Source: 2022 H1 AF Legal Presentation

AF Legal currently represents 2% market share in the Family Law market. This is quite small and creates an opportunity to grow the business even in a declining market.

The Family Law market is extremely fragmented with no national players. AF Legal reports they are the largest player in the space. With AF Legal being the only national player.

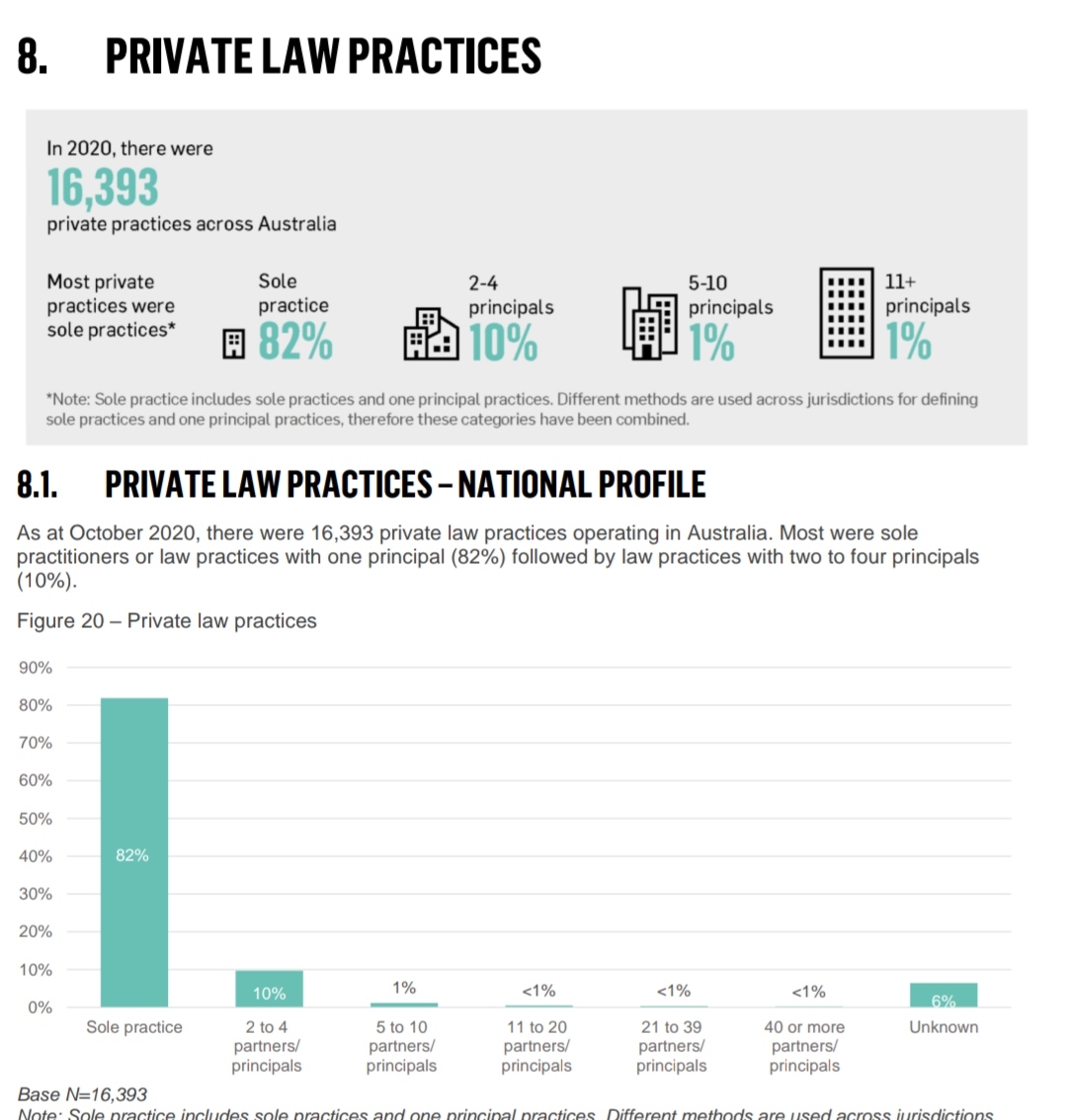

According to the URBIS national profile of solicitors 2020 report there were a little more than 16000 private law practices in Australia. Of the 16000 private law practices 83% are sole practitioners and 93% are below 10 practitioners in a practice.

Chart: URBIS national profile of solicitors

Those numbers collaborate with AF Legal. This fragmentation is great for AF Legal as they’ll be able to easily find acquisition targets for a long time to come.

All these small competitors give AF Legal another advantage. As the largest firm in the family law space they’ll be able to charge less than the competition by spreading out accounting, IT and other support service costs to many more cases and employees. This is also called economics of scale advantage.

Data: 2021 market update presentation AF Legal

AF Legal cites their 3 year target to achieve 10% market share in the Family Law market in Australia. This is great but how about after that?

AF Legal is already on top of that as they are looking to expand outside the Family Law market into the personal legal market. The personal legal market is even larger than family law at 7b AUD. Family law is one of the many types of law including in the total personal legal market. Other areas where AF can expand to are property law, injury, class action, and estate planning.

Chart: 2021 market update presentation AF Legal

AF notes that the markets under the personal legal market umbrella are fragmented like family law with no major players. Already in the last presentation on H1 2022 they have indicated they are looking to acquire firms outside the family law market. I also consider these other ancillary markets as complimentary. If I have a divorce with one lawyer but maybe I also have an estate matter why not use the same lawyer for both.

The opportunity in the family law market and the personal legal market should ensure lots of future growth potential for the firm.

Acquisitions

AF Legal is attacking this market opportunity through aggressive acquisitions. The multiples being paid for these businesses are very attractive multiples of 1.5-3.5 times EBITDA or 3-7 times FCF.

I review the last five

| Date | Firm Acquired | Purchase Price | Revenue | Interest Acquired | EBITDA Multiple | FCF Multiple |

| 1/31/22 | Withnalls Lawyers | 894K | 2.5M | 51% | 2.8-3.5 | 5.6-7 |

| 07/05/21 | Kordos Lawyers | 1M | 2M | 100% | 2-2.5 | 4-5 |

| 03/11/21 | Watts Mccray | 3M | 6M | 100% | 2-2.5 | 4-5 |

| 12/1/20 | Strong law | 350K | 1M | 100% | 1.4-1.75 | 2.8-3.5 |

| 06/01/19 | Nita Stratton Funk | 400K | N/A | 100% | 1.7 | 3.4 |

These multiples are quite cheap and show that management is quite disciplined with their acquisitions and not willing to overpay. Also AF goes for tuck in acquisitions which tend to be smaller than 10% of their current business. This is opposed to transformational acquisitions which I would say start at above 30% of the size of the current business. Tuck-ins are much safer due to being not as large. Due to the large fragmentation of all target markets AF should be able to continue buying up attractive tuck ins.

Organic Growth

AF is not all about acquisitions as there has been quite a lot of organic growth.

Below I look at recent Organic Growth

| Date | Area |

| 09/08/21 | North Canberra |

| 11/16/20 | Bundall, Gold Coast |

| 11/12/20 | Preston, Melbourne |

| 10/20/20 | Perth, Western Australia |

| 07/16/20 | Adelaide, South Australia |

| 06/15/20 | Maroochydore, Sunshine Coast |

| 06/15/20 | Caloundra, Sunshine Coast |

In the last two years they have opened 7 offices organically. Through acquisition another 4 were added. Organic growth tends to be a higher return on capital activity than acquisition based growth though a little riskier. AF Legal seems to be practicing a balanced approach.

Returns on Capital

AF Legal’s organic and acquisition led growth has led to AF Legal growing fast since listing revenue and ebitda CAGR are 50% and 125% per 2021 annual report. All this growth wouldn’t matter if the capital used wasn’t earning a sufficient return. Over the past two years AF Legal has achieved a 16% ROIC and 15% ROE. ROIC is a unlevered return while ROE is a levered return. The fact that ROIC is higher than ROE is due to AF sporting a high cash balance. These metrics compare favorably against publicly traded peers and speak to a good management team. I use a 3 year average ROIC and ROE for the firms below.

| Ticker | Firm | ROIC | ROE |

| K3C | K3 Capital | 2.45 | 0.551 |

| KEYS | Keystone Law | 0.40 | 0.280 |

| GTLY | Gateley Holdings PLC | 0.26 | 0.340 |

| AFL | AF Legal | 0.16 | 0.15 |

| IPH | IPH | 0.14 | 0.197 |

| CRAI | CRA International | 0.14 | 0.257 |

| FCN | FTI Consulting | 0.14 | 0.201 |

| QIP | Qantm Intellectual Property | 0.12 | 0.182 |

| SHJ | Shine Corporate | 0.05 | 0.102 |

| SGH | Slater and Gordon | 0.02 | 0.042 |

| DWF | DWF Group PLC | -0.15 | -0.039 |

Source: Data Collected from Company Annual reports

On top of that AF Legal has actually been increasing their return on capital metrics since IPO. Per H1 22 report ROIC is 23% increasing from 2019 levels of 8%. These increasing returns on capital line up with the new Executive Chairman Grant Dearlove taking office in Jan 2019.

| Year | H1 2022 | 2021 | 2020 | 2019 |

| ROIC | 23% | 20% | 11% | 8% |

Source: AF Legal Presentations

Management

In evaluating management I like to see their incentives when it comes to their executive comp. In the case of AF Legal they don’t have any set KPI’s or metrics that they tie to compensation. This leads to a vague compensation plan. The management team does have a 22% interest in the company so this satisfies management having a vested interest in making the stockholders money. Also total executive comp in 2021 was 1.4M vs the value of the stock interest in 2021 being 10.2M. This comes out to their stock ownership being around 7 times their compensation. Both the total insider ownership and the stock value to compensation indicates that the management team is incentivized to see the stock succeed. The vagueness of the compensation plan will likely rectify as the company becomes larger. Another interesting fact is that the Chairmen Grant Dearlove was head of Growth at Shine Corporate(ASX:SHJ) another publicly listed law firm so he has experience scaling publicly listed law firms.

Google Reviews

The business and management seem great but what do the customers think? Satisfying customers is the main driver towards a great business. I collected google review data from all AF Legal’s Offices with reviews to try to see if customer satisfaction lines up with business results. Seeing what the customer thinks is probably the best way to tell if the business is actually good.

Google Reviews

| Firm Brand | Location | Review Stars | Number of Reviews |

| Australian Family Lawyers | 411 Collins St, Melbourne VIC 3000, Australia | 4.2 | 33 |

| Australian Family Lawyers | 49 Octavia St, Mornington VIC 3931, Australia | 4 | 1 |

| Watts McCray Lawyers | level 15/370 Pitt St, Sydney NSW 2000, Australia | 4.2 | 43 |

| Watts McCray Lawyers | 1/9 George St, Parramatta NSW 2150, Australia | 4.1 | 9 |

| Australian Family Lawyers | level 5/40 Creek St, Brisbane City QLD 4000, Australia | 4.7 | 11 |

| Australian Family Lawyers | Tower 2/55 Plaza Parade, Maroochydore QLD 4558, Australia | 5 | 2 |

| Australian Family Lawyers | Level 27, St Martins Tower, 44 St Georges Terrace, Perth WA 6000, Australia | 4.7 | 23 |

| Australian Family Lawyers | AMP building, Level 6/1 Hobart Pl, Canberra ACT 2601, Australia | 4.6 | 5 |

| Australian Family Lawyers | Ground floor, 121 King William St, Adelaide SA 5000, Australia | 5 | 1 |

| Withnalls Lawyers | 22 Harry Chan Ave, Darwin City NT 0800, Australia | 2.8 | 4 |

Source: Google Reviews: Data as of 4/16/22

Overall I was able to find 10 of their locations with reviews out of a total of 17 firms. Alot of AF Legals office’s are rather new so it makes sense that not all of their offices have reviews. Almost all were highly rated with the sole exception of the Withnalls Lawyer with a 2.8 Star rating. The average rating was 4.3 stars with a total of 132 reviews. I think this shows that customers are happy with the company’s service and that the business results are not just smoke and mirrors.

Risks

Every Company has risks and for AF Legal I identified acquisitions, expansion into new areas of law, and the declining family law market as the biggest risks.

Acquisitions

As AF Legal strategy is to acquire a lot of firms to grow, the risk is if something goes wrong. Either not enough due diligence on a deal or a loss of key personnel could blow a deal. The fact that their acquisitions are tuck in and not very large should help to mitigate such risks.

Declining Market

AF’s main market, which is divorce, has been declining since 1976. Obviously never great to have the main driver of your market declining. A decline in the volume of cases could lead to reduced revenue in the future. The volume of divorces however has been on a very gradual decline which should be manageable. Also pricing looks to be outpacing the volume declines. AF is also planning to expand in other legal markets to grow.

Expansion into New Areas of Law

AF has done great in their area of family law at least according to google reviews and the company’s performance. To expand their TAM AF is looking to go into other legal markets. The risk is that they won’t have the same success in these other markets. One thing that will help is through acquisition. They could acquire a firm with lawyers with years of experience in those other markets which should limit this risk.

Valuation

For AF legal I’ll compare a Best case, base case, and fish out what the market is implying with the current stock price (Worst Case).

Valuation Table

| Worst Case | Base Case | Best Case | |||

| Current Market Cap | 34M | Current Market Cap | 34M | Current Market Cap | 34M |

| 2022 Underlying NPATA | 2.8M | 2022 Underlying NPATA | 2.8M | 2022 Underlying NPATA | 2.8M |

| Current P/E | 12 | Current P/E | 12 | Current P/E | 12 |

| Market Implied Growth Rate10YR CAGR | 2% | Forecasted Revenue Growth Rate 10 YR CAGR | 17% | Forecasted Revenue Growth Rate 10 YR CAGR | 26% |

| 10 YR Revenue Target | 28M | 10 YR Revenue Target | 110M | 10 YR Revenue Target | 214M |

| 10 Year PM Target | 10% | 10 Year PM Target | 12.5% | 10 Year PM Target | 15% |

| 10 YR Underlying NPATA Target | 2.8M | 10 YR Underlying NPATA Target | 14M | 10 YR Underlying NPATA Target | 32M |

| PE | 12 | PE | 20 | PE | 20 |

| 10 YR Projected Market Cap | 34M | 10 YR Projected Market Cap | 280M | 10 YR Projected Market Cap | 640M |

| Projected Return | 10% | Projected Return | 23% | Projected Return | 34% |

Market Implied

Using Benjamin Graham growth formula which is PE=2G+10 we can fish out the implied growth rate. The market is implying a 1% CAGR at the current stock price. So far AF has blown this number out of the water and I expect that to continue. AF Legal has 5M in cash so at the current stock price the market is implying that this is wasted or that it should be returned to shareholders. This seems harsh considering the excellent return on capital metrics achieved so far. This could also be the case of the market not believing the pro-forma or adjusted for acquisition run rate NPATA. I haven’t found a reason to doubt management as statutory revenue growth has been excellent and the company is generating operating cash flow. The return also assumes that AF is returning most of its capital back to shareholders to obtain that return. Either way you slice it the current market price seems excessively pessimistic. This is probably due to the current market downturn seen across global stock markets. AF is 12% off its market high price of .63 cents a share once accounting for dilution.

Base Case

The base case implies a return of 23% annualized which is quite impressive but may still be conservative. For one the 110M revenue target in ten years is actually management’s 3YR target. Management has made clear their 3YR target of 10% market share in the family law market which would be 110M in revenue. If management can achieve that then the base case would be blown out of the water. However I used 110M as a more consevative target in case things didn’t go as planned. Another thing is margins as the company becomes larger there will be more opportunities to share resources across firms increasing the margin opportunity for the company. In the base case however I assume no margin expansion from the current 12.5%. Finally the multiple for a company growing over 10% a year using Graham’s formula should be a 30-50 PE ratio. Especially in the services sector where multiples can be rich. I use a 20 multiple to be conservative.

Best Case

In the best case scenario management executes on their three year market share target in family law and continues to grow revenue either in the family law market or another legal market at a 10% CAGR. I also assume a little margin enhancement along the way to 15% PM. This implies a 34% annualized return.

Summary

As the base case and best case scenarios illustrate AF Legal has the potential to deliver fantastic returns over time becoming a multibagger opportunity. AF Legal has a large TAM that can continue to increase as they move into new markets. AF Legal has a history of high growth and high increasing returns on capital. The future looks bright for AF.