Airtel Africa 2023 Update

Introduction

I review each position in my portfolio on a yearly basis and now it’s time for Airtel(AAFRF). In my last article I highlight how Airtel Africa, a telecommunications and fintech company operating in Africa, is poised for significant growth driven by increasing mobile penetration, data usage, and the expansion of mobile banking services in the continent. With a focus on its largest market Nigeria, Airtel has substantial room for growth, benefiting from favorable demographic trends and low levels of mobile and data usage compared to other emerging markets. Its financial performance, includes high revenue growth and rising return on invested capital (ROIC). The company also has Airtel Money the third largest mobile money platform in Africa.

However it seems a mistake I made in my first article was not looking at the currency risk hard enough. The devaluation of the Nigerian Naira by almost 100% against the USD has had a significant impact on Airtel’s financials, causing revenue growth to turn negative and foreign exchange losses to mount. While Airtel continues to demonstrate growth in key performance indicators (KPIs) and operates in a region with substantial growth potential in mobile penetration, data usage, and mobile money, the ongoing currency devaluation and regulatory challenges in Nigeria pose uncertainties. As a result, I have become uncertain about whether to hold, sell, or add to my position.

Currency Devaluation

Since my last article on the company the devaluation of the Nigerian Naira from 460 USD/NGN to 770 USD/NGN as of now. An almost 100% devaluation against the dollar. With this backdrop the company’s Q1 2023(as of June 23) revenues were still 10% higher given the currency headwinds. However if the quarter closing rate of 752 NGN/USD was used to calculate revenue, revenues would have declined by 4.4%. Also the company reported a $471M foreign exchange loss which sent profit after tax negative to $-151M.

Source: TradingView

The currency had been overvalued for a while as the black market had been trading “within N714/$ and N680/$ for cash transactions” back in November of 2022. You would think after a freefall like the Naria has experienced that the currency might stabilize but the black market is still trading at a 20% discount to the actual rate at around 980 USD/NGN. Other factors weighing on the currency is the high inflation rate Nigeria is experiencing which has hit an 18 year high and the current account to GDP being negative now for four years. Due to these factors the currency is probably set to continue to devalue.

The currency has already had a large effect on Airtel’s financials with revenue growth going from 9.6% to -4.4% YOY. Over the course of the year the effect of the currency will be even larger, per management in the Q1 2024 press release

The annualised impact of the devaluation in Nigeria incurred in June 2023, assuming no further devaluation for the remainder of the year, is expected to be between $850m and $900m on annualised revenues and between $450m and $500m on annualised EBITDA, with the large majority of the impact expected to materialise in Q2’24 and the remainder of the fiscal year. “

If those projections come true this would represent a 20% drop in revenue and EBITDA from last year for FY 2024.

Regulatory Challenges

Now all these numbers for Airtel don’t include any price increases. This sounds like a good thing as maybe the company could offset the impact of the devaluation, but in reality its not as the regulator doesn’t seem like they want to play ball. All price increases for telco services must be approved by the Nigeria Communication Commission(NCC) and they have been reluctant to do anything. In May of 2022 ALTON (Association of Licensed Telecommunication Operators of Nigeria) which represents the large telecom players in Nigeria proposed a 40% price increase which didn’t go anywhere. The NCC then allowed a 10% price increase around September of last year only to back off a month later. The reluctance of the regulator to allow price increases is another kick in the gut for Airtel. The telecom industry contribution to GDP hit 16% in Q2 2023. You would think that the regulator wouldn’t want to hamper such an important industry in the country?

Performance

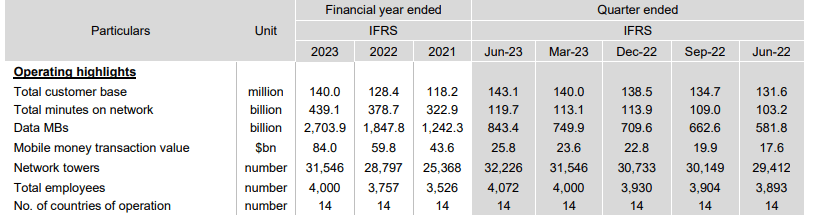

Now in terms of growth in key KPI’s the company is still doing well.

Source: Airtel Africa Q1 2024 IR Pack

As you can see the company is still growing customer count, minutes on network, data MB’s and mobile money transactions. This growth is exactly why I like the company as its positioned to benefit massively from the opportunity in Africa due to the low mobile and data penetration there.

Looking forward though, the company has been able to grow even while the currency has depreciated. Since 2018 the Nigerian Naira had depreciated around 30% from 357 USD/NGN to 460 USD/NGN. Yet in the same time Airtel had grow revenue 84% in USD. So this does inspire confidence that the company can get back to growth.

| Fiscal Year | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 |

| Revenue | 5,268M | 4,724M | 3,919M | 3,439M | 3,103M | 2,863M |

| USD/NGN ending March | 460 | 415 | 378 | 385 | 360 | 357 |

Conclusion

This brings me to the tough question of what to do with my position here. On the one hand the company is in a long term secular growth story as Africa increases mobile penetration, data usage, and mobile money. On the other hand the currency shows no sign of letting up and the regulator isn’t being very accommodative.

Because of this uncertainty I don’t think I will be adding to my position in Airtel and might look to exit if we don’t see any relief when it comes to the currency or the regulator. Based on FY2023 EBIT the company is trading at 7 times EV/EBIT which is quite cheap however FY 2024 EBIT will most likely be alot lower and FY 2024 EV/EBIT will be around 9-10 times. Still kinda cheap especially if Airtel can get back to growth in FY 2025.