Frontier Development(LON:FDEV) 2024 Annual Stock Review

I purchased Frontier Development last year off the back of a return to higher profitability in 2025 as the company was having a bad 2023 due to high development costs and the overall downturn in the video game market. I also assumed revenue would be flat to 2025 as the release of new titles and sticky back catalog sales would keep sales flat. And overall I thought the stock was cheap at £3.41 a share.

Where to begin with the troubles?

- Age of Sigmar Warhammer a new IP the company released had bad reviews and underperformed dramatically.

- The new F1 Manager 2024 did not perform well when released however the reviews are good.

- Operating Margins in the FY 2024 report were way worse than I thought they would be.

- Revenue in the FY 2024 report declined way more than I thought it would.

I was thinking about selling Frontier after the bombing of the Age of Sigmar title which was only a month or 2 after my purchase where I was down almost 70% from my cost basis. But then I saw insiders purchasing shares so I decided to hold on and see if they know more than me. Results were still terrible yet the share price doubled since 12/23.

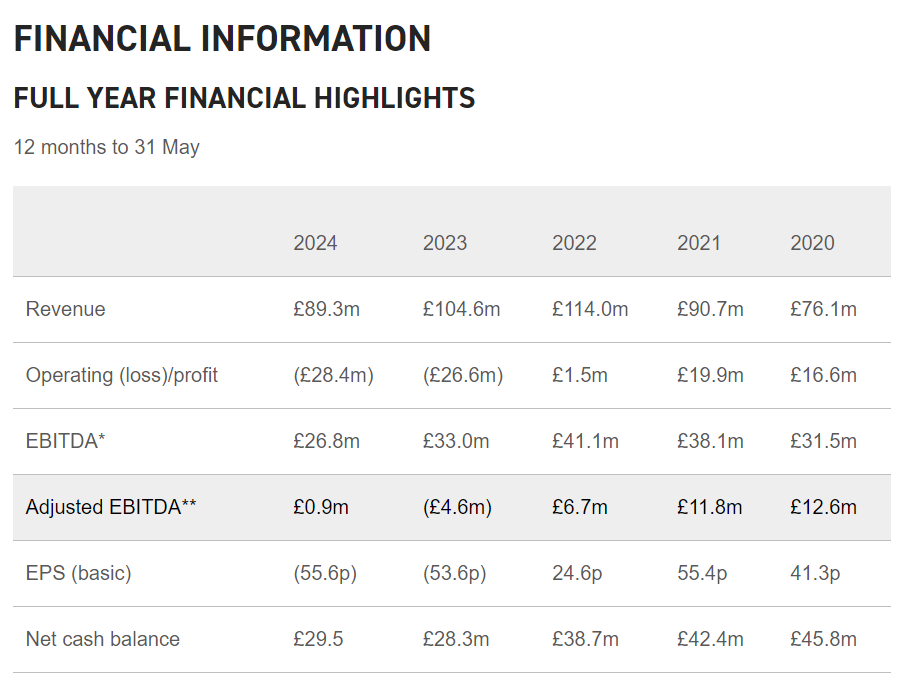

The FY 2024 revenue for Frontier was down from £104M to £89M and Operating Profit was slightly down to -28M.

Source: Frontier Development

Positive’s and Looking to the Future

- Even though Operating profit was very negative, FCF was breakeven. Which means cash on the balance sheet has been flat for the year. This ensures the company still has a good balance sheet.

- Expenditure on intangibles is way down. Which in one sense is bad cause thats the company’s video game development and maybe future revenue will be impaired. But on the other hand amortization on intangible assets will be lower next year barring impairments. Profitability in FY 2025 will probably be higher than 2024. However I think my forecast in my first article of 20% OP in 2025 is not gonna happen.

- The company has reduced operating costs by 20% from 2023(Layoffs)

- Moving from developing new titles and publishing to refocusing on sequels of older titles with large audiences already. Planet Coaster 2 was released in FY 2025 which is late 2024 and Jurassic World 3 releasing with a new movie in 2026. This is good in the sense that new releases should have better sales numbers because their not altogether new titles like Age of Sigmar Warhammer. These sequels should also cost less to develop than the brand new titles of Age of Sigmar Warhammer and F1 Manager 21.

- The 2022 and 2023 years for the video game market were declining to flat years for the industry as people began to go outside after covid and play less games. 2024 will return the video game market to its long term growth trend. Specifically PC gaming is back and is where Frontier has the majority of its revenue.

Frontier’s new game Planet Coaster 2 was released on 11/6/24. The game so far has mixed reviews but its still early. On Steam the game has 2628 reviews as of 11/9/24 and there are a lot of complaints about bugginess and not as much content as the first game and a more recent game Planet Zoo. The bugginess is not great but seems to be standard for new releases these days and the content is probably the company planning DLC’s already. 2628 reviews in 3 days is already more reviews than F1 Manager 2023 and Warhammer Age of Sigmar which were both released last year. The first Planet Coaster has over 50K reviews on Steam which if that correlates to sales means Planet Coaster 2 could bring a big sales uplift in FY 2025.

Not to mention that in FY 2026 the company is planning to release a third Jurassic World Game which was another big seller in the past with alot of reviews. These combined releases coupled with the reduction of operating costs and a decline in development costs which will lead to lowered amortization expense makes me pretty optimistic about FY 2026 results. For FY 2025 I expect some revenue uplift as the video market is growing again so the back catalog should do good and sales growth from Planet Coaster 2. And with the lower expenses I expect operating profit to at least break even assuming no write downs.

For FY 2026 I expect that’s where we’ll see a return to 20% operating profit and over 100M of revenue if it ever will happen. With the stock at a £90M market cap and closely tracking a multiple of 1 times sales, those results could lead to a big stock price appreciation.

With that said video game releases are not easy and with the Jurassic World property you are also dependent on the movie performance which is being released simultaneously with the video game. So risk is high but the company still maintains a decent balance sheet in the gaming space and can take a hit if a game doesn’t work out. Due to the risk I think it’s a hold for me for now.

I’ll look to Sell If

- This years operating profit doesn’t improve significantly

- Revenue continues to fall in FY 25

- Insiders give up and start to sell shares