Published 03/10/2023

Grupo BMV(BMV:BOLSAA): South of the Border

Introduction

Grupo BMV or Bolsa Mexicana de Valores SAB(BMV:BOLSAA) is the largest financial exchange in Mexico and the second largest in Latin America. Grupo BMV operates in six different business segments: Equities, Derivatives, Information Services, OTC, Capital Formation, and Central Securities Depository. The company is a stable high quality business with great returns on capital and a fantastic balance sheet. However, BMV is trading at a 50% discount to peers. At the current price, I’ve added the company to my portfolio due to the stability of the business, high returns on capital, and attractive valuation.

Businesses

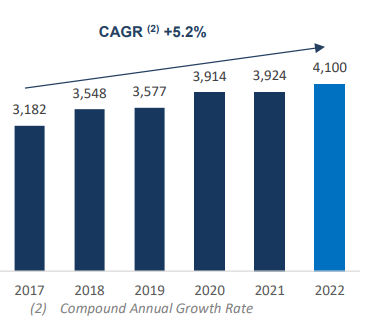

Grupo BMV has grown revenue MXN 5.2% CAGR and 4.2% in USD since 2017.

Growth has been uneven in Grupo BMV’s operating segments with some segments growing much faster than others. Grupo BMV operates in six different business segments: Equities, Derivatives, Information Services, OTC, Capital Formation, and Central Securities Depository. Below I summarize each segment.

Equities

This segment includes fees from equity trading and CCV(Central Counterparty Clearing) which is used to offset risks that may arise from certain transactions. Since 2015 growth has been 3% in constant currency. This doesn’t tell the whole story as revenue peaked in 2018 and hasn’t eclipsed that since. 2019 was a downturn for the Mexican market as well as the first year of the left-wing president AMLO. Which I think both contributed to the loss of revenue for Grupo BMV in 2019. Since then the market has recovered and so revenue has come back to but not eclipsed 2018 levels.

Revenue in Equity Segment(In Millions)(MXN)

| Year | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

| Revenue | 532.00 | 518.34 | 529.40 | 485.23 | 552.87 | 475.53 | 480.51 | 428.08 |

Developments

Below are a number of recent developments that characterize the Mexican equity markets both good and bad.

Competition: A new Mexican stock exchange was founded in 2018 called Bolsa Institucional de Valores (BIVA). They have captured market share, going from 0-22% as of 2022. I’d say this is a negative.

Anemic IPO activity: There are only 134 Mexican stocks trading on the exchange as of 2023. This is a decline from 141 in 2017. This compares to Brazil which has 271 listed stocks and from 2018-2021 had 81 IPO’s. The decline in stock listing especially compared to Brazil is a negative.

Poor Mexico: Porfirio Diaz once said “Poor Mexico. So far from God and so close to the United States.” About 18 Latin American blank-check companies have been listed in the U.S. in the last three years(Link). Mexican companies could just list in the American exchanges which have higher liquidity. This would obviously be a negative going forward.

Fintech: Starting in 2015 Mexico reformed its banking sector which allowed fintech companies to start sprouting up. As of 2022, Mexico has over 512 fintech start-ups. In the coming years, the IPO market in Mexico may come to benefit from this growing sector. This would be a positive for the future.

Market Cap to GDP: This measure looks at the size of the stock market compared to the real economy. This is a crude metric that can be used to see potentially how many more companies could list on the stock market if the ratio is under 100%. Mexico’s Market Cap to GDP as of the end of 2022 was 33%. This compares to the US at 156%, Brazil at 51% and Chile at 60%. The low ratio speaks to the opportunity for more firms to be listed in Mexico in the future. This is a positive.

Retail Investors: Since 2018 individual investment accounts in Mexico have grown from 242k to 4.5M in 2022. Mexico still has room to grow as the US with a population of 334M has 121M investing accounts. Which is 36% of the population. Using the same ratio in Mexico would give Mexico 43M accounts. More individual investing accounts will lead to more volume in the market which is a positive for the future.

Pension Reform: A new Mexican Pension bill was passed in 2020 which will increase Employer contributions from 6.5%-15% by 2030. This will increase the amount of money flowing into the Mexican Market. This is a big positive.

Expansion: the company owns a percentage of the Peruvian Stock Exchange. The Peruvian stock exchange in its 2020 investor presentation mentions being interested in being acquired. As a part owner already this could be a potential route for expansion. The other smaller Latin America exchanges could also be areas to expand in the future. This is another positive.

Weighing the pros and cons I think the future growth potential of the Mexican market will outweigh the negatives of increased competition and the recent poor IPO market. Either way, the equity segment is only 13% of the entire company.

Derivatives

This segment includes MexDer for trading in swaps and futures and Asigna for clearing and settlement of derivatives. This segment brought in 223m in revenue in 2022 which is around 5% of the group’s total revenue. Due to the small size, I didn’t look into it that much.

Information Services

One of Grupo BMV’s fastest growing segments is its information services segment which includes Valmer and market data products. This is Groupo BMV’s third largest segment accounting for 17% of revenue in 2022. Valmer provides market data to users to help in the valuation of financial products. Market data is sold through BMV, Mexder, Sif Icap, and Valmer depending on the data being sold. Revenue has grown from MXN 329m in 2015 to MXN 692m in 2022. Which is an 11% CAGR in constant currency and around 7% in USD.

Revenue in Information Services Segment(In Millions)(MXN)

| Year | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

| Revenue | 692 | 630 | 603 | 546 | 468 | 428 | 379 | 328 |

Data users like passive funds, quants, and HFT’s(High-Frequency Trading) are becoming increasingly prevalent in financial markets which ensures this segment should continue to grow fast into the future. Users of Groupo BMV’s data have increased from 129 in 2016 to 205 in 2021.

OTC

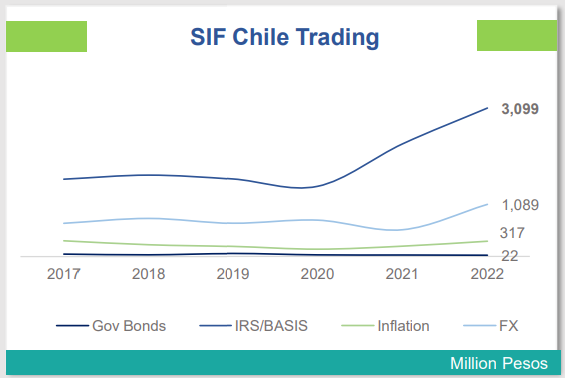

The OTC segment accounts for 18% of the group’s revenue. The OTC market operates through SIF ICAP. SIF ICAP is a joint venture with ICAP, a British firm with more than a quarter century’s experience, considered the largest inter-dealer broker in the world. SIF ICAP is a inter-dealer broker that operates in Mexico, Peru, and Chile. SIF ICAP derives most of it’s revenue from trading in government bonds with over 70% of revenue coming from Chile.

Revenue has grown from MXN 435M in 2015 to MXN 736M in 2022, which is a 6% CAGR in constant currency and 3% in USD. This segment is heavily dependent on the volume of government bonds, interest rate swaps, and FX derivatives traded for growth, specifically Chile’s. I don’t really know why volumes in Chile has been increasing so much other than volatility in inflation and interest rates.

Capital Formation

The capital formation segment includes debt and equity issuance. This segment is the only declining segment for the reasons mentioned in the equity segment(Poor IPO market and Debt). Capital formation revenue has declined from 577m in 2015 to 492m in 2022. However, capital formation peaked in 2018 at 694m. The year before the downturn for the Mexican market as well as the first year of the left-wing president AMLO.

Revenue Capital Formation Segment(In Millions)(MXN)

| Year | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

| Revenue | 492m | 498m | 579m | 614m | 694m | 654m | 603m | 577m |

I expect this segment to get back to growth as liquidity at the exchange improves over time and equity performance returns.

Central Securities Depository

The largest segment is the Central Securities Depository called Indeval which makes up 31% of the group’s revenue and is a fast grower. This segment is responsible for the custody, deposit, clearing, and settlement of all securities on the stock exchange including stocks, debt and foreign securities. Which basically means they transfer ownership of a security from the seller to the buyer. From 2015-2022 revenue has increased from MXN 516m to MXN 1271m which is a 14% CAGR in constant currency and 10% in USD.

Revenue Central Securities Depository Segment(In Billions)(MXN)

| Year | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

| Revenue | 1.27B | 1.28B | 1.22B | .994B | .886B | .681B | .539B | .516B |

Within this segment, there are four sub-segments with the two largest being the Global Market Services and Local Custody segments. In the Local Custody segment, the key KPIs are total assets under custody and average daily settlement.

Both settlement and custody have been growing with government debt being the largest of both. The Mexican debt market has the highest volume traded of any emerging market with $640B being traded in 2021. This is almost a 3x from 2016 which was $222B. The reason for all this trading volume is due to Mexico’s close proximity to the US and the low US interest rates of the last decade. The high Mexican interest rates compared US interest rates make it an attractive target for the carry trade. With the spread of the 10YR Mexican bond over 5% higher than the US 10YR Bond. Due to this, growth in volume should continue.

The Global Services Segment handles the SIC(International Quotations System) which provides trading of stocks and ETFs not listed in Mexico. For this segment, BMV provides custody and settlement for the SIC. The number of securities available to trade in the SIC has increased from 1779 in 2018 to 2763 in 2022. SIC is over half the volume of the Mexican Stock Market. Theirs still an opportunity for continued growth as worldwide there are almost 9000 ETF’s and this shows no signs of stopping.

Number of Exchange Traded Funds Worldwide

Returns On Capital

A sign of a great business is their return on capital metrics and Grupo BMV delivers. Grupo BMV’s ROE and ROIC have been high and stable over the past 5 years with ROE averaging above 20% and ROIC above 30%. ROIC is higher than ROE due to the company having no financial debt and a large net cash balance. This conservative balance sheet makes it even more impressive that the company is generating such high returns on capital.

| Year | 2022 | 2021 | 2020 | 2019 | 2018 |

| ROE | 21.21% | 20.66% | 19.73% | 18.95% | 21.30% |

| ROIC | 40.2% | 37.3% | 36.2% | 32.3% | 35.3% |

Management

In evaluating management I looked at executive comp, returns on capital, and past acquisition multiples.

I found it kinda hard to evaluate management comp as I couldn’t find exact executive comp metrics. From what I could find about management in the 2021 annual report

- 60% of total compensation is variable

- long-term retention plan can make up 20% of the compensation deferred over five years

Both of the above compensation details I would say are good however they don’t disclose what metrics they are using to evaluate the performance of management. Not knowing the metrics means I don’t know the incentives which is a negative.

As I looked at in the above section Grupo BMV’s return on capital metrics is quite stellar and stable. So management must be somewhat competent.

Googling both the CEO and CFO didn’t bring back anything negative so that’s a positive checkmark.

Finally, I looked at past acquisitions which were mostly done in 2008.

- Indeval: 2008

- 15 to 12 times earnings

- Grown quite a lot since 2008 I’d rate this a A+ acquisition

- Other: 2008

- This Included Asigna, PGBMV, and CCV

- BMV paid 1.6B MXN in 2008 for the three companies above. In the year after the acquisition they took a 500M Write Down.

- I estimate that these combined acquisitions brought in MXN 80M-50M a year

- That means the multiple paid for the assets was between 20-30 times

- Considering the multiple paid, the write down, and the anemic growth of the derivative segment which Asigna is apart of I don’t think this turned out to be a good acquisition probably a D

The last acquisition I could find was in 2014 with BMV purchasing shares in the Peruvian Stock Exchange. I could not calculate the multiple for this.

Regardless of these acquisitions the company’s CEO José-Oriol Bosch Par who started in 2015 after all these acquisitions had been made has not made any large acquisitions since coming in. Instead he has grown the payout ratio including dividends and buybacks from around 60% to close to 90% in 2022. So it seems that Jose has been rather conservative with the cash flow of the business.

To conclude I think management is neutral, since the new CEO cash flow has been given back to shareholders rather than spent on acquisitions. Before the current CEO, management had a mixed record. However, I couldn’t really evaluate management incentives when it came to compensation.

Valuation

In terms of Valuation BMV is trading at a 50% discount to other financial exchanges. BMV(Ticker:BOLSAA) is trading at 11 times P/E while other exchanges like SGX(Ticker: S68) trade for 20 times and the Nasdaq trades for 30 times earnings. This discount may be attributed to BMV operating in an emerging market. An exchange that I didn’t include below GPW the polish exchange also trades at around a 10 times multiple(also kinda interesting). Another reason for the low multiple compared to peers could be the relatively low revenue growth of 5% over the past 3 years. However the Japanese(Ticker: JSE) and Australian (Ticker:ASX) Stock Exchanges also both had low revenue growth but are trading at twice the multiple.

| Ticker | P/E | 3YR Revenue CAGR |

| NDAQ | 30.02 | 12% |

| OTCM | 14.91 | 20% |

| CBOE | 60.59 | 18% |

| CME | 28.67 | 5% |

| ICE | 21.71 | 14% |

| TW | 28.16 | 18% |

| ASX | 24.40 | 0% |

| X | 21.97 | 6% |

| BOLSAA | 10.97 | 5% |

| DB1 | 49.28 | 13% |

| ENX | 15.13 | 30% |

| LSEG | 23.22 | 72% |

| JSE | 20.44 | 4% |

| S68 | 19.02 | 7% |

Side Note: All revenue growth measured in local currency

Even with those two items I think BMV is a good value at the current price. A multiple of 11 doesn’t imply much growth but if higher growth were to return to Mexico because of some type of boom then there is a good chance of multiple rerating. Also other exchanges with low growth trade at higher multiples so its possible BMV could rerate even with the same growth they managed the past five years. Also, over the past five years the payout ratio including buybacks and dividends has averaged between 60%-80% which would imply a 6-8% shareholder yield which you can get paid while waiting for higher growth or multiple rerating.

Conclusion

In conclusion, Grupo BMV has multiple different segments growing at different speeds with mostly bright futures especially if the equity markets get a boom. BMV is trading at a 50% discount to peers which I think makes it rather attractive. As the business is high quality with great returns on capital, fantastic balance sheet, and a management team that probably won’t light money on fire.