Piquadro Group – Expensive Bags, Good Business?

Piquadro is a luxury Italian leather company operating under three brands Piquadro, The Bridge and Lancel. The company designs and partially manufactures its own goods while selling directly in its own stores and wholesale. The company is trading cheaply, has doubled revenue in the last 6 years and has high insider ownership still being run by its founder. Even though the luxury market has taken a hit in 2024, Piquadro has been able to continue its growth. Piquadro seems attractive here and I’ve added it to my portfolio.

The Company

Piquadro was founded in 1998 by Marco Palmieri because he saw a gap in the market between super cheap leather products and extremely expensive bulky briefcases. First though Palmieri actually founded an industrial control company called Mediacom and ran that for around 10 years before selling it and founding Piquadro. The first Piquadro store was opened in 2000 and since then as of 2023 the company has grown to 88 stores. Not huge store growth but it is a luxury brand. The company claims all its leather comes from the fine Tuscan tanning district. Marco is still the leader of the company and owns 68% of the outstanding shares.

Looking at the website a backpack would set you back $300-$700. And Piquadro Luggage sets you back $400-$1200. The brand has a focus on leather goods, bags and travel items and actually sells more to men than women. Piquadros biggest competitor at least according to reddit is Tumi the high end luggage brand owned by Samsonite.

When trying to assess Piquadro as a brand I looked at Trustpilot and the brands store Google reviews. Currently on Trustpilot the brand has a solid 4.2 stars with 227 reviews. Looking at the brands stores in Italy it looks like on average stores are above 4 stars which is solid.

The brand manufacturers a lot of its own leather goods as it partially owns a factory in China which as of 2023 manufactures 25%(which it is my understanding the factory only manufactures for Piqadro and not the other brands) of the companies turnover which Piquadro is 43% of the companies turnover. This implies over half of Piquadros inventory is manufactured by the company. Though the company has been pushing a made in Italy marketing and claims to be making more stuff in Italy though its unclear how its doing that. Though in the companies 2024 presentation they list owning 2 manufacturing plants in Italy but I can’t find how much of their goods they sell are made in those factories.

Piquadro is the company’s most profitable segment and has grown rev from 2016 from €70M to €81M as of 2023 and EBIT from €5.5M to €12.2M(the EBIT per brand is an estimate as I allocate shared expenses base on revenue). This is a 2% revenue CAGR but a 12% EBIT CAGR. The majority of Piquadros revenue is from Italy at 70% of sales which represents an opportunity to grow in foreign markets.

Source: Chart created by author, data from company annual reports

Piquadro became a group in 2016 after the acquisition of The Bridge, another leather goods company in Italy. The company paid €3.1M for 80% of The Bridge with an option to buy the remainder in 2021 based on revenue targets for an all in amount of €5-6.2M with the option. The company added €8.4M in debt from the Bridge which brings the EV to 14M. Revenue in the first year of ownership was €24M which puts the purchase multiple at .6 times EV/Sales which is quite cheap. The Bridge is also a bag brand but with a bigger focus on purses and bags for women than Piquadro being more male focused. But both brands have similar product categories. The Bridge was a loss making company when Piquadro initially purchased it and has since been turned around and is a profitable segment for the company.

The Bridge since 2017 has grown revenue from €24M to €34M but more impressively grown EBIT from €.8M to €3.9M in 2023.

Source: Chart created by author, data from company annual reports

The last company under the group’s umbrella is Lancel which was acquired in 2018. Lancel was founded over 140 years ago and is based in France with operations globally but focused on Europe. The brand is also in the bag space. Looking at their website the brand seems to be mostly focused on handbags for women though more flashy than The Bridge. A quick look at the website shows bags costing from $500-$1500. The acquisition price was an earnout of 20% of the next 10 years profit up to 35M euros. But I’m confused as Lancel came with a net cash position of 43M. Which implies Piquadro got the company for free. Though I guess it was because Lancel was losing money pre acquisition and the former owners, luxury brand company Richemont just wanted to get rid of it.

Since Acquisition in 2018 Piquadro has been able to successfully turn around Lancel. Going from €45M of Revenue and -€14M of EBIT to €64M of Revenue and -€1.4M of EBIT. The brand is still the least profitable brand of the group but Lancel has been the most growth focused of the brands. Since Acquisition DOS(Directly Owned Stores) stores have grown from 62-69 in 2023.

Source: Chart created by author, data from company annual reports

The company seems to be a distressed company investor with its purchases of The Bridge and Lancel and so far they seem to be good at turning around those luxury brands. In 2021 Piquadro tried to buy another brand Sergio Rossi however they were outbid by a chinese company. Palmeirei, the majority owner and founder mentioned in an interviewer that the company is certainly looking for more acquisition targets in the luxury space, specifically other Italian or French brands. Also he is focused on continuing to grow the current brands organically, specifically in China and second tier cities in Europe as people in Europe move away from large cities into the smaller ones.

Financials

In terms of overall company financials the company has more than doubled revenue since 2016 from 76M to 180M as of 2023.This was mostly on the back of acquisitions but also from organic growth. Out of the overall increase in revenue of 104M, 41M is organic and 63M is from acquisitions. This puts the company at a 7% organic growth CAGR.

Source: Chart created by author, data from company annual reports

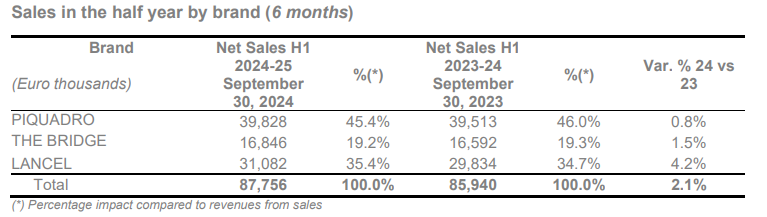

So far this year the company has been able to increase revenue 2% and EBIT 12% under the backdrop of weak luxury demand reported by LVMH and CPRI and others. Piquardro might be less impacted by the macro because it positions itself in the middle luxury instead of super high end and due to its bag. Also luggage and bags make up a big chunk of the company’s current revenue and is probably more correlated with travel than luxury. It’s unclear whether or not Piquadro will be able to continue to outperform the industry.

Source: Company H1 2024/25 release

ROIC for Piquadro is better looked at at the brand level as Lancel drags down the company ROIC. Using the companies disclosed fixed assets per brand as a proxy for invested capital you can see that both Piquadro and The Bridge have great ROIC of over 30%. Lancel having negative EBIT is the exception however the company has made strides in increasing profitability so eventually the group could be able to turn Lancel into its other brands.

Source: Chart created by author, data from company annual reports

Last but not least the balance sheet. The company has very little debt and ex leases their cash almost covers their liabilities.

| Year( In Millions) | 2023 | 2022 |

| Current Assets | 117.74 | 127.54 |

| Cash | 35.09 | 52.94 |

| Total Assets | 179.94 | 192.06 |

| Current Liabilities | 78.34 | 80.19 |

| ST Debt | 9.70 | 12.90 |

| LT Debt | 5.70 | 14.40 |

| Total Debt | 15.4 | 27.3 |

| Total Leases | 40.59 | 41.09 |

| Total Liabilities | 115.23 | 131.01 |

| Liabilities Ex Leases | 76.64 | 89.92 |

| Liabilities Ex Leases and Cash | 41.55 | 36.98 |

| Total Shareholder Equity | 64.72 | 61.06 |

Valuation

The company is trading at 10 times 2023 EV/EBIT. Considering the company is growing in 2024 with EBIT up 12% in 2024 the company will be even cheaper after this year’s full year results. The company has been growing organically 7% since 2016 with the Lancel brand being the strongest grower. The company still has an opportunity to increase profitability as the Lancel brand as of 2023 was unprofitable and the other two brands have high ROIC. The weak luxury environment may be a good thing for the company as it may create an opportunity to acquire another luxury brand on the cheap as the company has successfully done twice before.

If the company pays out half their earnings the dividend will be around 5-6% while if the company can continue to grow at a 4-7% CAGR then your return would be around 9-13%. This doesn’t include any acquisitions nor any multiple rerating which is definitely likely if the company can continue to grow as other luxury companies trade at double the multiple. The company is quite small at 100M market cap so that may be a reason why it trades at such a low valuation.

Risks

Luxury Sector Takes a Hit

The luxury sector in general seems to be experiencing a downturn which may affect Piquardros short term performance. Companies such as LVMH, CPRI, Moncler, and Kering, big players in the luxury space have all reported YOY declines. Not even Gucci has been spared as the brand is down 18% YOY as of H1 2024. The luxury companies are blaming this on weak consumer demand which is also affecting other sectors such as restaurants which I wrote about here. Whether this is just the start of a recession or not, this short term decline in the otherwise long term uptrend of luxury goods sales fueled by China’s demand and the increase of millionaires and the global wealthy will most likely be short lived.

China

China is a big player in the luxury market and is a big growth driver for most of the big brands. Piquardro is planning to open a number of stores there to drive more sales. If China decided to invade Taiwan it may not be great for Piquadro or the luxury market in general.

Perception of Brand

Perceptions of brands come and go. Micheal Kors used to be a luxury brand. But oversupply of the brand has hurt the brand image and the brand has been struggling for years. Ralph Lauren, a brand that was struggling in the late 2010’s has been reinvigorated and has regained a place in the luxury hierarchy in recent years. If any of Piquadros brands are mismanaged or consumer tastes change this could negatively affect the brand.

Conclusion

The Piquado group is a luxury distress turnaround specialist already turning around one company and on the path of turning around the second. With a CEO who is ambitious and who has a large stake and thus incentive to create value for shareholders. The company is trading

Key Metrics

For every investment I’ve been setting metrics to evaluate companies in my annual reviews. For Piquadro I’ll track revenue, EBIT per brand, DOS, and revenue outside Europe.

- Revenue

- EBIT per brand

- DOS

- Revenue outside Europe