Science Group: Cheap UK Consulting Acquirer

Science Group(LON:SAG) is a UK listed company involved in R&D, regulatory, compliance and defense consulting while also involved in DAB radio chips and atmosphere management systems on submarines. The variety of businesses were brought to the company through acquisitions beginning in 2013. The business seemed to change significantly in 2010 when the current chairman bought a significant stake in the company and shortly after made the companies first acquisition. The company is sitting on an excellent balance sheet with high returns on capital and only a 12 times EV/EBIT.

Currency

The company is listed in the UK so I will need to buy Pounds to invest. As a US based investor the currency could have an effect on my returns so I must evaluate it. I looked at the Pound in my article on Frontier Development and for the most part my opinion hasn’t changed much. To summarize, given the Pound’s overvaluation and the ongoing negative current account balance in the UK economy, I anticipate a 2% depreciation in the Pound against the Dollar in the future, which could potentially offset returns on my investment. All the companies financials are in Pounds and all numbers below are in Pounds but the company does receive a lot of revenue in Dollars and Euro’s.

The Business

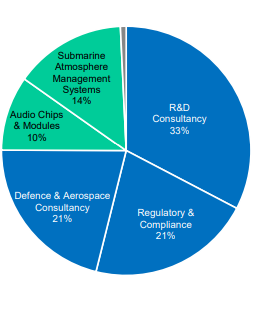

The Science Group operates in 5 primary segments these include

- R&D Consultancy

- Regulatory and Compliance

- Defense consultancy

- Audio Chips

- Submarine Atmosphere systems

Source: 2023 Interim Presentation

R&D Consultancy

R&D consultancy includes the subsidiaries Sagentia Innovations, Leatherhead food research and Oakland Innovation. These companies primarily advise in the medical, food and beverage and chemicals industries. Within these industries the subsidiaries advise on numerous aspects such as designing medical devices, introducing new technologies or methods into the manufacturing process, conducting market or consumer studies for product development, and creating a process to reduce waste in a companies manufacturing process. This was the company’s largest segment representing 33% of revenue. Sagentia Innovations was the original company pre the acquisitions in 2013. Both Leatherhead and Oakland were acquired in 2015. Leatherhead was acquired for 1.6M with 8M in revenue however it was a money loser at the time and Oakland was acquired for 4.5M net cash and had 3.5M in rev and .4M in profit leading to a multiple paid of 11 times.

The Regulatory and Compliance

The Regulatory and compliance segment includes the subsidiaries of TSG consulting and Leatherhead food research. The companies this segment advises are mostly in the chemical and food & beverage sectors. Core services include advising clients on food regulation across the world as they go international, food label compliance, government approval advice for a variety of chemicals in the US. This segment makes up 21% of the company’s revenues which makes it tied for third largest. TSG consulting was acquired in 2017 for 14M which had revenues of 16M and a net loss of 1.1M.

Defense Consultancy

The Defense Consultancy segment includes the newly acquired TP group. This segment makes up 21% of the company’s revenues which is tied for third with regulatory and compliance. Examples of what TP group does is assessment of customers GBAD network, developing a assessment framework for the maritime operations centre, and creation of a should cost model to analyze military purchasing costs. TP group was acquired in 2023 for 30M which annualized I estimate the company brought in pre acquisition 38-48M in revenue and 1-2M in operating profit. I think defense consulting could prove to be very interesting given the war in Ukraine and pledges of various European governments to increase defense spending by large amounts.

Products Segment

The last two segments I’ll bundle together as the products segment. This includes the submarine atmosphere system and the audio chips. The subsidiaries here are TP group and Frontier communications. This segment is 24% of sales as of H1 2023. Frontier was the Sciences group’s first product based rather than consulting company. It was probably brought more for its R&D center rather than the manufacturing. Frontier was acquired in 2019 and is focused on the design and manufacturing of DAB radio chips. DAB is one of the 2 european digital radio standards. Basically digital radio is an upgrade to the old FM and AM radio that most people are familiar with. Digital radio is projected to be a growing market into the future at over a 10% CAGR. And I suppose most of the growth from digital radio will be the eating of FM and AM market, as a 2021 study in Ireland showed that 77% of radio listening adults listen to FM radio still. All in Frontier cost the company 14M and was a struggling company which in the year it was purchased did 21M in Revenue with a net loss of 7M. Fast forward to 2022 and the company seemed to be turned around with 24M in Rev and 3.6M in EBITA. However the first half of 2023 was terrible for the subsidiary but consumer electronics tends to be volatility sector.

Finally the Submarine atmosphere segment was a part of the TP Group acquisition. This segment has been rebranded as CMS2. The systems that the subsidiary designs and builds generate oxygen while removing and managing other gases in the submarine. This segments profitability is quite low and so is TP group in general and the strategy no doubt will be to restructure the business. And I wonder if the rebranding might signal a desire to sell off this part of the business while keeping the defense consulting.

Overall

The group’s primary strategy seems to be to buy underperforming consulting businesses in related areas to the companies current business and turn them around. For example the original business Sagentia Innovations in 2010 was a small unprofitable consulting business when Martin Ratcliffe purchased a large interest and began turning the business around. By 2017 the company had increased revenue by 150% and had a 15% operating profit. This growth is impressive when you take into the fact that little equity was issued and it was financed through cash flow. Though they did issue equity for their latest acquisition for TPG Group. It’s kinda hard to know what is organic revenue vs acquired, however in the next section I’ll attempt to extract that. Overall the company seems to have been successful in this strategy at least when you look at the financials.

Financials

The company has grown revenue from 2015 from 31M to 86M as of 2022. And EBITA from 5M to 16M. This is growth in Rev of 16% and EBITA of 18% CAGR. H1 2023 revenue is already over 20% higher than 2022 mostly due to the TP group acquisition.

Source: Author created chart, data from company reports

It’s hard to distinguish what is organic and inorganic growth. The company discloses the dividends subsidiaries pay to the parent and this could be used as a proxy for organic growth. Sargentia paid 3.5M to the parent in 2015 and by 2019 paid 7M. After 2019 covid happened and the dividend was canceled but inferring from the data from 2015-2019 organic growth in the main business seems quite good. Also in the companies annual reports, in the intangible asset section the company makes forecasts on the future revenue growth of the subsidiaries for impairment testing. In the 2022 report the 5YR forecasts range from .2% for Frontier to 9% for TSG with the main business segment the R&D segment forecasted to do 4.6%.

Source: 2022 Annual Report

So its fair to say that the majority of the growth of the company comes from acquisitions but at least its good to know that the companies already under the Science Group umbrella are growing organically and are not shrinking ice cubes and management is hiding it with acquisitions.

The most important thing though is not growth but returns on that growth. The Science Group checks the box here too as the company has excellent ROIC averaging over 20% from 2015-2022 and ranging from the mid teens to high twentys. The dip in 2019 was due to the acquisition of Frontier which was struggling at the time of purchase and was very unprofitable.

Source: Author created chart, data from company reports

The growth of the company has not come at the expense of the balance sheet and the company has a very good balance sheet. As of H1 2023 the company has 29M in cash compared to 57M in total liabilities. However only 14M of those liabilities is actually borrowings with the majority being accounts payable. The debt is secured by 2 properties owned by the company which as of 2021 were estimated to be worth between 20M-30M. So once accounting for the companies cash, real estate and accounts receivable the liabilities can easily be covered.

Source: Author Created Table, data from company reports

Insiders

Martin Ratcliffe is chairman of the board and the largest stockholder in the company with a 20% share. Martin seems to be the instigator over the company’s current strategy as he bought a sizable stake in the business in 2010 and began the current growth strategy of acquiring and turning around businesses which has proven to be successful so far. Martin Ratcliffe is in his early 60s which means he probably could keep this going for another 10 to 20 years. He has sold shares though most recently in 2020. However this is understandable as he probably wanted to monetize some of his investment considering how well the stock price has done since his buy in. Overall I think insiders are incentivized and have generally done good.

Valuation

In terms of valuation 2022 AEBIT came in at 16M. The current market cap for the company was 170M at the time of writing and the company had 29M in cash with 57M in liabilities. This gives an EV of 200M which puts its EV/EBIT multiple at 12 which seems quite cheap with the growth and returns on capital the business has produced. I estimate the current share price of the stock could return from 10-17% CAGR in the long term.

I estimate 7-10% growth from acquisitions which is about half the growth generated from acquisitions in the past so this is a conservative number. Also the company being only 170M market cap is quite small so finding acquisition targets should be quite easy still. 2-5% from organic growth which is in the range of what the company is forecasting for their segments. Then 1-2% return from buybacks and dividends as about 3.5M combined was returned to shareholders in 2022 which at the current share price would be a 2% yield however the buybacks which made up 1.3M of that may not always be that high so I made the range on the low end to be 1%.

Source: Author Created Table, data from company reports

A 10-17% return is quite attractive especially since this does not include any multiple expansion which could definity happen since the company is only at a 12 times multiple.

Risks

The main risk to the investment is the acquisition based strategy of turning around acquired businesses. If management gets over their skis and overpays for an acquisition or fails to turn the business around the returns may be lower than I suspect going forward. Compounded on this is that management likes bigger acquisitions than say a tuck in. TP group the latest acquisition by the Science Group was doing annualized 40-50M in business compared to the entire company which did 86M of rev in 2022. So not getting an acquisition right when it’s such a large addition to the existing business adds extra risk to the thesis. The company does have quite a good balance sheet however which should mitigate this to some extent.

Update 4/3/24

After writing the article I went to purchase the stock on IBKR assuming since it is LSE listed that It would show up but apparently some small LSE stocks aren’t available through IBKR. So even though I like the company it looks like I won’t be able to add it to my portfolio.