Sutl Enterprise: Set for Growth

Introduction

Sutl Enterprise is a marina operator that derives most of their revenue from their ONE°15 Marina Sentosa Cove in Singapore which they own and operate. They also manage various other marina’s and are in the works to manage and construct others with an emphasis in Asia. Sutl Enterprise is a great play on the rise of the super wealthy in Asia as they will need a place to park their yachts. The company is at a very attractive valuation with more cash than market cap and trading at less than 10 times normalized earnings.

Macro

According to the 2021 State of Yachting Report Asia’s ownership of superyachts stands at 6.8% as of 2021. This is exceedingly low as 59% of the world’s population lives in Asia. Not only that but if we look at the number of millionaires in just Japan, China, India and Australia these four countries hold 20% of the number of millionaires in the world. As millionaires are the main buyers of Superyachts the amount and the growth of millionaires shall correlate to increased demand of yachts and thus marinas. Asia looks to be the highest growth area in the world in terms of GDP according to the World Economic Form for the foreseeable future. The number of millionaires and thus the demand for Yachts and a place to put them should only grow.

Number of Millionaires by Country (2021)

| Country | Number of Millionaires | Percent of World Population | Percent of Population of Country |

| United States | 21,951,202 | 39.1 | 8.8 |

| China | 5,279,467 | 9.4 | 0.5 |

| Japan | 3,662,407 | 6.5 | 3.5 |

| India | 697,655 | 1.2 | 0.1 |

| Australia | 1,804,644 | 3.2 | 9.4 |

| Indonesia | 171,740 | 0.3 | 0.1 |

| France | 2,468,939 | 4.4 | 4.9 |

| Germany | 2,952,710 | 5.3 | 4.3 |

Another bullish macro area for Sutl Enterprise is that there seems to be a lack of supply for marinas. For example in Hong Kong there are over 10,000 private vessels yet only 5,000 public and private moorings. This seems to be a similar trend throughout Asia. I have not found exact numbers to quantify this supply and demand dynamic though.

To conclude Asia not only shall grow its demand of yacht consumption significantly in the future but there seems to be a shortage of marinas in Asia. As a marina operator in Asia with ambitions to build a string of marinas throughout. Both these factors will drive SUTL Enterprise forward.

Growth Prospects

SUTL Enterprise Marina brand is called ONE15. SUTL Enterprise seeks to expand this brand from the shores of Singapore to other countries around the world.

SUTL Enterprise has numerous projects in the works.

This includes

- ONE°15 Marina Nirup Island in Indonesia

- ONE°15 Marina Logan Cove Zhongshan in China

- ONE°15 Marina Taihu Lake, China in China

- Indonesia Navy Club managed by ONE°15 in Indonesia

They may also have a deal to own and operate a marina in Thailand but they haven’t talked about it in there annual report in a while so I assume it’s on hold. I have emailed management to see what they have to say.

The project nearest to completion is the one on Nirup Island expected to be completed in June 2022. However the conversion of the island to a luxury resort will not be done till the end of 2023. The two in China are being delayed due to the new shutdown in China.

It will be interesting to see how much revenue can be generated from these projects. It won’t be insane growth as to my understanding these are all management contracts and SUTL Enterprise won’t actually own any of these Marinas. I’ll be watching for any revenue step ups in the back half of 2022 after Nirup is operationally.

Insiders

Insiders own 54% of the company. I consider this to give insiders alignment with shareholders. Also in 2021 the company issued a special dividend of over 10 cents. This put their 2021 dividend yield over 20% rewarding shareholders greatly. One cause of concern is that the company is family run and employs a number of family members.

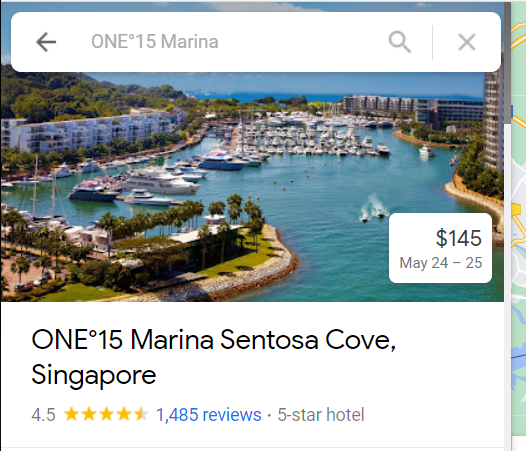

A way to see how good management is are the ratings of their operations.

Source: Google Maps

SUTL main marina in Singapore is very highly rated by google maps at 4.5 stars with over 1485 reviews. This inspires confidence in the Management of SUTL.

Risks

I see a number of risks to the thesis.

Family Control

The company is controlled by a family and thus could be used as a personal piggy bank.

No Growth in Marina‘s

Due to covid a number of their past projects were canceled or put on hold. Must notably was their ONE15 Marina project in Malaysia which is being canceled and the assets will be disposed of per the company. One of the keys of the thesis is for the company to grow the number of Marina’s. The risks are these projects may not get done or cost way more than expected affecting returns.

Valuation

SUTL is at a very attractive valuation as the market is currently valuing the company below its cash. The market cap of the company is at 41mm while the cash balance is at 47mm. The company has all this cash as it sells memberships in advance. These memberships are put in on the balance sheet as a liability however these memberships are nonrefundable and thus you could argue not a liability at all. Accounting for this the company is in a very solid financial position with no real debt and a very large cash position. This provides immense safety in the investment. Per management they keep all this cash to be able to seize opportunities to grow the business. As developing a marina can be quite expensive.

| Balance Sheet | |

| Cash | 47mm |

| Total Assets | 74mm |

| Liabilities | 22mm |

- Includes adjustments for Deferred Membership Income

SUTL is also generating net income and the company trades at less than 10 times normalized income.

| SUTL Enterprise Net Income(In Millions SGD) | ||||||

| Year | Average | 2021 | 2020 | 2019 | 2018 | 2017 |

| Net Income | 4.63 | 4.92 | 3.18 | 2.48 | 5.80 | 6.75 |

| Market Cap | 41.76 | |||||

| P/E | 9 |

The one thing wrong with SUTL is revenue growth which has been flat since 2017. However this is caused by covid and the economic slowdown asia was experiencing back in 2019. I expect long term revenue growth of at least 3% even if they cannot expand into new marinas.

SUTL has been paying the same dividend of 1.75m since 2017. This represents a 4.2% dividend yield which will reward shareholders as they wait for new developments.

Pre Covid the company was trading at higher valuation ratios than now with a share price averaging in the 60-90 cent range. The company is currently trading at 48 cents a share. This is mostly caused by the unfortunate macro events that have plagued the company since 2019 including covid and the economic slowdown Asia was experiencing back in 2019. This should rectify as the economics recover around the world.

SUTL Earnings Multiples

| Year | Current | Average | 2021 | 2020 | 2019 | 2018 | 2017 |

| Net Income | 4.92 | 4.63 | 4.92 | 3.18 | 2.48 | 5.80 | 6.75 |

| Market Cap | 41.76 | 51.68 | 46.43 | 35.84 | 49.93 | 58.58 | 67.65 |

| P/E Ratio | 8.48 | 11.16 | 9.44 | 11.27 | 20.13 | 10.10 | 10.02 |

Conclusion

In summary SUTL is trading very cheaply at below cash value, 9 times earnings, and a 4.2% dividend yield. As the economy comes out of covid the company should be able to deploy cash in growth opportunities and trade at a higher multiple. It’s hard to calculate an expected return on this investment however.