Published 1/6/2024

Aeroporto Guglielmo Marconi di Bologna (BIT:ADB) Annual Review

I review each position in my portfolio on a yearly basis and now it’s time for Aeroporto Guglielmo Marconi di Bologna(BIT:ADB). ADB is the operator of the Bologna airport in Italy. In my last article I wrote how ADB was set to eclipse 2019 PAX numbers by 2023 and recover from covid. And as it turned out I was correct as of Q3 2023 PAX is up 7.5% vs 2019. This PAX increase is mostly due to low cost carriers growth as legacy carriers are still down nearly 20% from 2019 levels. Though PAX and Revenue have recovered from covid, profitability is still lagging. Overall I think ADB is still a good company and I’ll continue to hold going forward.

Key Metrics

As I’ve been doing in my other annual reviews I keep track of 4 key metrics to make it easier to evaluate the performance of a company and know when to buy and sell. For ADB the metrics I think are important are PAX, Rev, Profit Margin, and Rev per PAX.

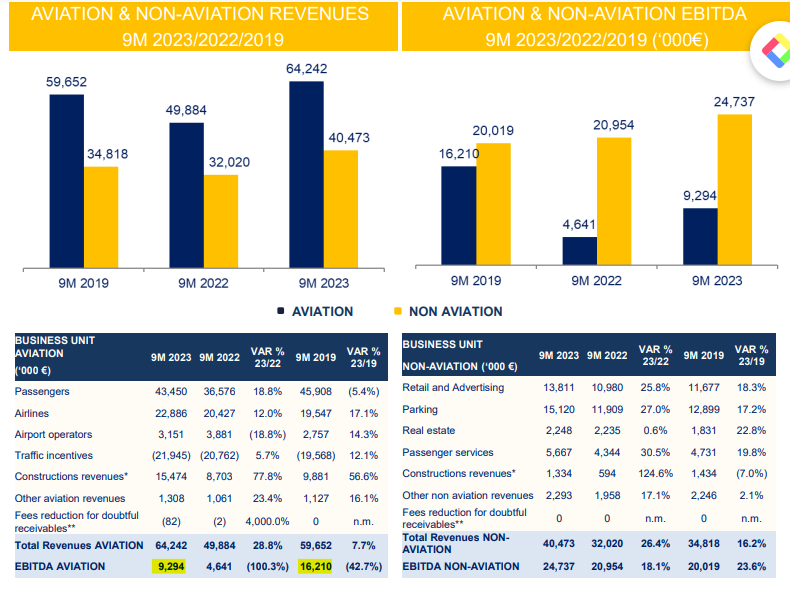

| Year | Q3 2023 YTD | Q3 2022 YTD | Q3 2019 YTD |

| PAX | 7.7M | 6.5M | 7.2M |

| Revenue Ex Non Aero | €87.8M | €72.6M | €83.2M |

| PM | 14% | 14% | 19% |

| Rev per PAX | €11.4 | €11.2 | €11.6 |

Both PAX and Revenue look good coming into Q3 2023 which are up 18.7% and 20% from last year and 7.5% and 5.5% from 2019. This is despite total European PAX still being -3.1% below 2019 levels. Margins though are still lagging. Management blames the mix between low cost and legacy airlines and cost pressures. In particular Aviation margins are well below 2019 levels. Going from 30% EBITDA margins in 2019 to 14% in 2023. This could partially be explained by the decreased rev per PAX as ADB has lower aeronautical charges than in 2019 and also lower aeronautical revenue than in 2019. Also Ryanair the airport’s major airline earlier this year signed a 6 year agreement with ADB. This could be why aero charges and thus EBITDA margins went down this year. Nevertheless this is a positive as it lowers the risk of Ryanair abandoning ADB. In 2024 we’ll probably see some relief here as the new airport charge table goes into effect which in general increases prices by 10%ish though it looks like passenger charges declined to offset that somewhat.

Source: ADB 2023 Q3 Presentation

Overall 2023 has been a solid year though weaker than I expected from my last article but much better than peers. I’m also confident that profitability will improve. Also fun fact the airport has a Lamborghini Huracán that guides planes on the runway.

Holding

Net Income will probably come in around €17-€18M which would put the current multiple at 16-17 times earnings. Which isn’t super attractive, especially when looking at the Mexican airports. However the bet is still on margin expansion as there is still a 3% spread on margins compared to 2019. At 2019 margins the company would have made €22M in income pushing the PE down to 13 which is much more attractive especially given the airport has very little debt. Though if you look at margins between 2014-2019 the average was 13% which is 1% below what the company is coming at this year. So maybe I was too aggressive before. I had thought margins might be sustainable due to the fact it had been almost increasing every year between 2014-2019 and as airports gain more PAX they gain more sales leverage. Another negative is that the dividend has yet to be reinstated. I’ll probably continue to hold and only look to sell if I find a better idea and I hit my 90-100% fully invested target.