Published 1/6/2024

Grupo Aeroportuario del Centro Norte (OMAB): A Bet on Nearshoring

Introduction

Grupo Aeroportuario del Centro Norte ticker OMAB is a Mexican airport operator with its most significant asset being the Monterrey airport. Monterrey is the second largest metro area in Mexico and is also the industrial hub of Mexico known for manufacturing steel, cement and auto parts. Due to its manufacturing focus and its proximity to the American border the city should benefit from the nearshoring trend. In addition to Monterrey, OMAB manages 12 other airports, collectively generating passenger traffic equivalent to that of Monterrey, making Monterrey a major component of the company. With a track record of high returns on capital, growth in passenger numbers, and a promising outlook, OMAB appears to be well-positioned for a favorable future, all at an attractive valuation.

Macro

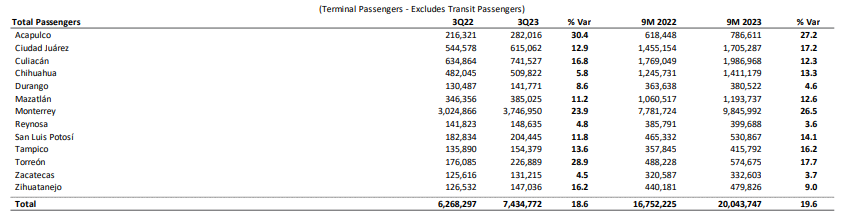

OMAB was granted the concessions of 13 Mexican airports in 1998 for 50 years after the government decided to privatize them back in the 90s. Monterrey is the company’s most important airport accounting for 48% of PAX as of Q3 2023.

Source: OMAB Q3 2023 earnings report

Monterrey is the second largest metro area in Mexico, trailing only Mexico City with around 5.1M people, representing a remarkable 24% growth since 2010. That’s even faster growth than the Dallas Metro area and Texas which in my article on Bank7 are some of the fastest growing areas in the US. Recognized as an economic powerhouse, Monterrey hosts nine of the top fifteen most globalized Mexican companies. Manufacturing dominates the city’s landscape, constituting over 30% of the GDP of Nuevo Leon, where Monterrey serves as the state capital. Primary sectors include automotive manufacturing, aerospace, steel, cement, and home appliances.

Given this industrial focus, business travel accounts for the majority of OMAB’s passenger traffic. Monterrey stands out as a prime beneficiary of the nearshoring manufacturing trend due to its skilled workforce and close proximity to the United States. Also if you believe Boston Consulting Group Mexican labor is actually cheaper than in China(though probably not in Monterrey). Notably, since 2021, Nuevo Leon’s government has reported 164 new companies announcing investment plans in the state, with Tesla’s $5 billion factory being the most significant and well-known addition. The state anticipates nearly doubling its foreign investment compared to 2022, contributing to the surge that saw new investment in Mexico reach 48% of foreign direct investment in 2022, marking the highest since 2013.

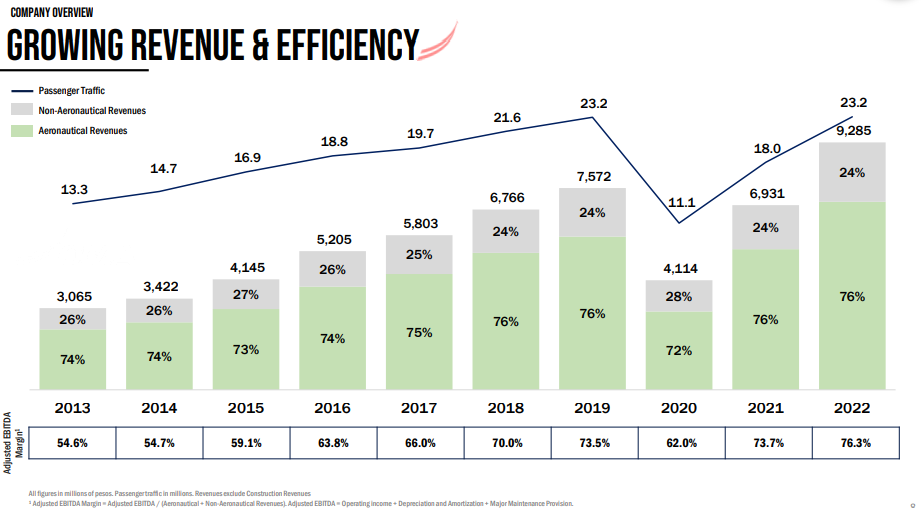

Not only should OMAB benefit from the growth of Monterrey but also the Mexican airline industry in general. OMAB has grown PAX from 2013-2019 at a 10% CAGR from 13.3M to 23.2M. Along with the overall Mexican market which grew from 61M to 102M in the same period at a 9% CAGR.

Source: OMAB Q3 2023 Presentation

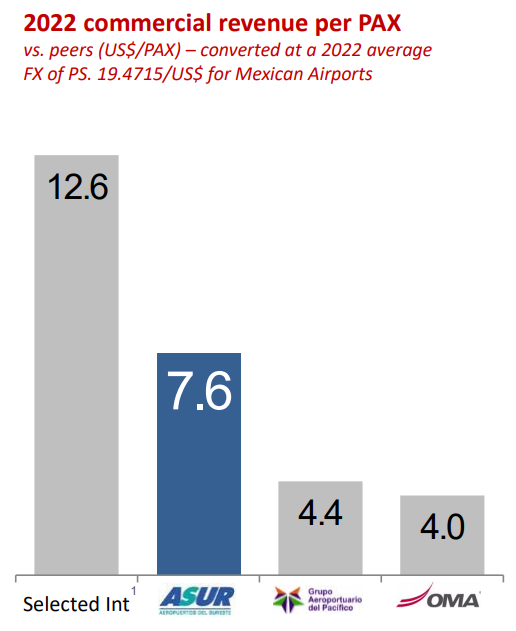

The Mexican airports in general were also able to recover much quicker from covid especially compared to European peers. Even with this growth air travel per capita in Mexico is well below the United States and even Latin American peers Chile and Columbia. Mexico’s flights per capita is .48 vs Chilies of .93, Columbia .58 and the United States of 2.03. On top of that, commercial rev per pax in Mexico and at OMAB is well below international pricing. With international making $12.6 per PAX vs OMAB making $4.0. This means OMAB can grow faster than PAX as they raise prices.

Source: ASR Q3 2023 Presentation

In Boeing’s 2023 Commercial Market Outlook they forecast Latin America PAX traffic to grow by 5.5% over the 20 years 2023-2043. I expect Mexico and OMAB to grow faster than that.

Due to the trends of Nearshoring and the general growth of passenger travel in Mexico OMAB is set up for a long runway of growth.

Financials

Growth has been very profitable for OMAB. Revenue has increased by a 16% CAGR in MXN and 10% in USD from 2013 to 2022. Profit has followed close behind at an 8% CAGR. I expect this level of growth going forward as PAX continues to grow and the company raises prices.

Source: Author created chart and data from company annual reports

As of Q3 2023 the company is on track to grow YOY 19.6% in rev and 35.3% profits. In USD this is even higher growth due to a strong peso.

The company has maintained this growth with high returns on capital as since 2013 ROE has averaged 26%. ROE has grown over the years due to increasing leverage. The company has a D/E ratio of slightly over 2. This is an average amount of leverage for an airport as some European peers have D/Es over 3.

Source: Author created chart and data from company annual reports

Customer Reviews

I love looking at companies with physical locations because then you can see them on google maps and see the reviews. I look at customer reviews to see if a company is legit and if they’re making customers happy which I assume translates into continued growth and shows management knows what they are doing. I looked at OMABs top 5 airports by PAX. Which include Monterrey, Culiacan, Ciudad Juarez, Chihuahua, and Mazatlán. On average OMAB has great reviews with 4.4 stars with 44 thousand reviews in their top 5 airports.

A review by Abril noted the Monterrey airport had “Excellent service, clean, large with many stores for different tastes in all aspects, one of the best airports in Mexico, without a doubt.”

| Airport | Google Rating(As of 1/2/24) | Number of Reviews |

| Monterrey International Airport | 4.4 | 23,402 |

| Ciudad Juárez International Airport | 4.1 | 5,956 |

| Aeropuerto Internacional de Culiacán | 4.5 | 5,487 |

| Aeropuerto Internacional de Chihuahua | 4.4 | 6,039 |

| Mazatlán International Airport | 4.4 | 4,318 |

The favorable ratings received by their premier airports instill confidence in the competence of the management.

Risks

The primary concern for the company lies in the actions of the Mexican government, which holds the authority to grant concessions for new airports, posing a potential threat to OMAB by introducing competition at any given time. This could adversely impact any of the company’s nearby airports. An example is Aeropuerto Del Norte, another airport in the Monterrey area that sought permission to serve commercial aviation but was denied(at least for now). Additionally, the government has initiated the construction of a new airport in the state of Chihuahua, another area where OMAB serves. Both of these airports are owned by the government. Of particular concern is the Aeropuerto Del Norte, situated in Monterrey, OMAB’s most crucial airport. However, large cities can support multiple airports, as seen in Dallas and Milan, the short-term effects of new airport operations may be challenging, but given Monterrey’s substantial size and population growth, OMAB is likely to weather the storm in the long run.

Moreover, the government retains the authority to increase taxes and fees at any time, setting tariffs for airports. An example is the recent increase in the airport concession fee from 5% to 9%, coupled with a proposed reduction of airport usage fees by approximately 10%. Although OMAB currently charges 10% less than the maximum tariff allowed by law, these governmental demands may impact profitability.

The government’s inclination, under President Obrador, to take on more public service responsibilities, such as the military running a new airline in Mexico and overseeing operations at Aeropuerto Del Norte, indicates a shift away from private sector involvement. Instances like the majority ownership of a new airport in Chihuahua by the state government and the cancellation of a contract with Consolidated Water for a new water utility due to a preference for public management underscore this trend. Despite Obrador’s term concluding in 2024, and the one-term limit in Mexico, he is very popular and it is likely somebody from his party will win.

In summary, potential challenges stemming from new concessions, fee increases, and a government leaning away from private sector involvement constitute the main risks for OMAB.

Valuation

Depending on where you think the peso(assuming you’re buying the US listing) will end up the company is trading at a 12 to 14 times 2023 earnings. The concession fees could drive this somewhat higher next year unless growth offsets it. This is quite cheap for an airport as European peers trade for 20-30 times earnings. This is probably due to an emerging market discount but also because the European airports like Fraport(ETR:FRA) and Flughafen Zurich(SWX:FHZN) own their main airport outright while OMAB leases theirs. Nevertheless OMAB has much higher ROE then those two and much higher growth rates in PAX. OMAB shares this with the other two publicly listed Mexican Airports. The other two operators in Mexico PAC and ASR are also quite interesting but OMAB is the cheaper one out of the 3 and is most exposed to the nearshoring manufacturing trend. However both PAC and ASR are pretty interesting as well.

In terms of expected return, if OMAB can maintain a 20% ROE which has been closer to 30% in recent years and a 75% payout ratio which has hovered around 50% to over 100% since 2014. OMAB could provide a 11% IRR excluding multiple expansion. Considering the company’s growth prospects the company could get to a 20-30 times earnings multiple especially if nearshoring in Mexico creates more speculation in Mexico.

Conclusion

In summary, Grupo Aeropuerto del Central Norte emerges as an enticing investment within the Mexican aviation sector. With its focal point being the Monterrey Airport, the company strategically capitalizes on the city’s industrial prominence and its strategic location near the U.S. border, aligning effectively with the burgeoning nearshoring trend. OMAB showcases strong financial performance, sustained passenger growth, and positive customer acclaim. Despite potential governmental challenges, OMAB’s established presence in the Monterrey region, coupled with its appealing valuation, positions it favorably for investors seeking exposure to the opportunity arising from the trend of nearshoring manufacturing activities.