Published 01/20/24

Carriage(CSV): Return to Normal in 2024

Carriage Services operates within the death care industry, focusing primarily on funeral homes and cemeteries. The recent decline in the company’s share price can be attributed to various factors, including the unsuccessful merger attempt with Park Lawn a Canadian peer, challenges posed by interest rate headwinds, and normalization from covid. Despite these setbacks, the fundamental strength of the business remains intact, and the current valuation appears to me to be attractive. According to company management, the business is expected to stabilize by in 2024 and start to grow. Additionally, the majority of their debt is set to mature in 2029 which should shield the company from current interest rate headwinds. This combination of factors suggests to me this might be a time to dive in.

Industry

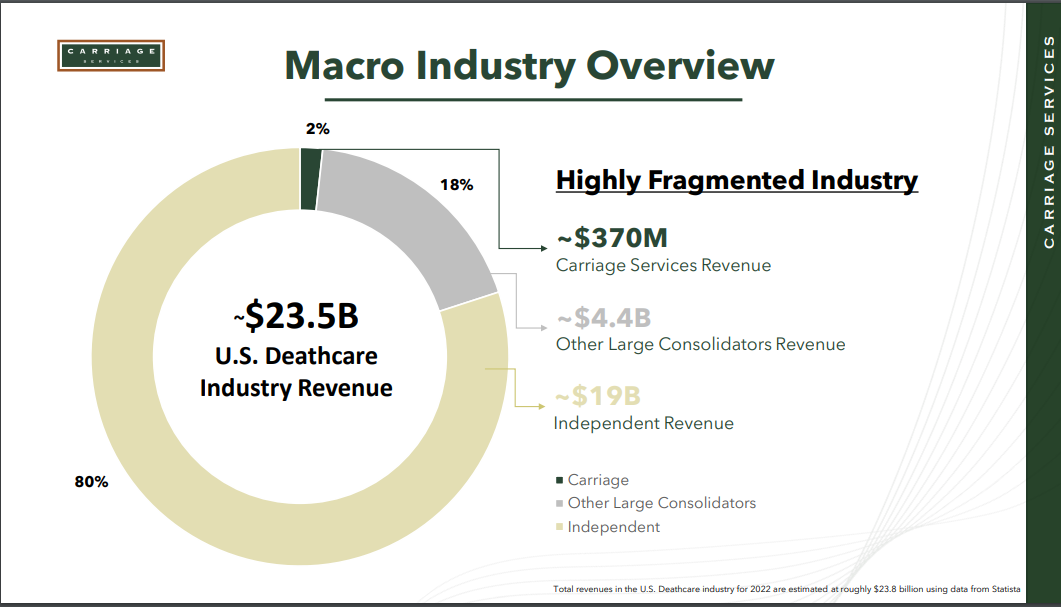

The funeral home industry where Carriage operates is a $19.2B industry as of 2022. The funeral home industry in the United States is highly decentralized, comprising over 19,000 establishments, with approximately 80% being privately owned, often characterized as small, family-run businesses. Despite being among the top three largest companies in the industry, Carriage Services, with a total revenue of 370 million, holds only a 2% market share, highlighting the vast opportunities for growth and consolidation in this market.

Source: 2022 Investor Presentation

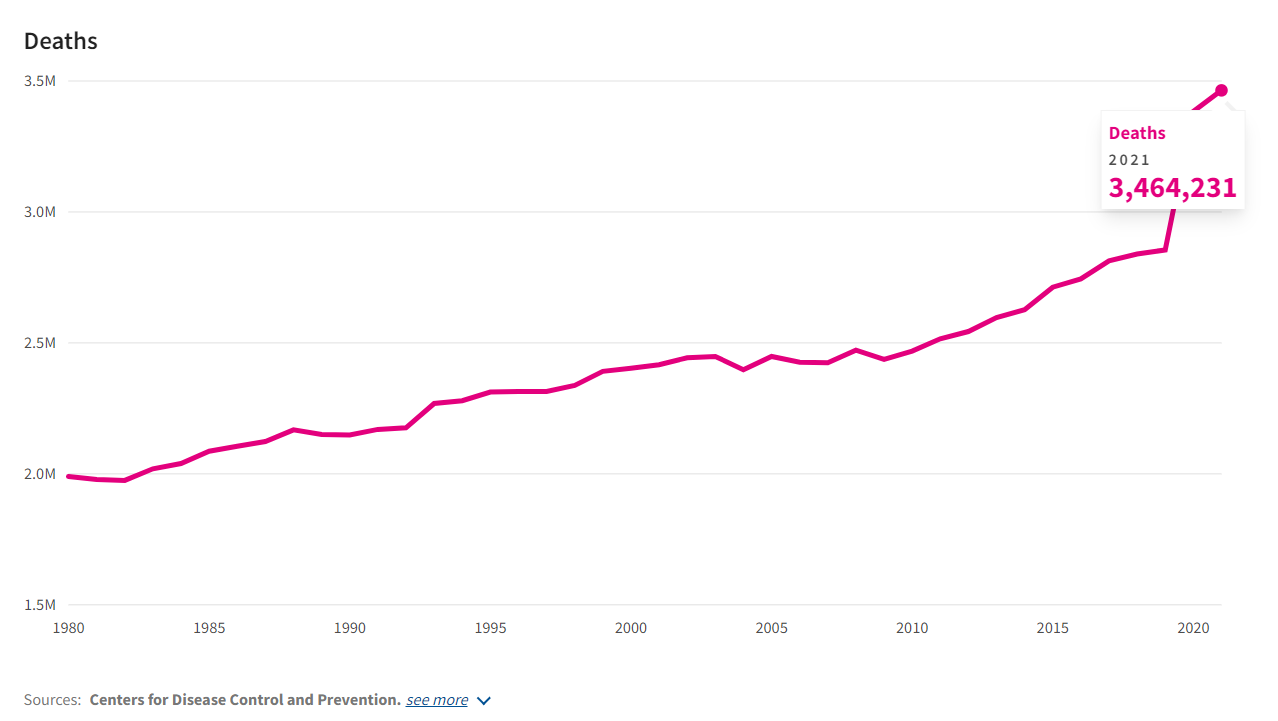

When I look at a company’s industry I always want to see growing volumes as a high tide lifts all boats and death is a growing industry. Total deaths in the US have increased from 1.9M in 1980 to 2.9M in 2019 about a 1% CAGR. This will continue to grow going forward as the UN projects an increasing death rate per thousand for the US going forward as there are over 70 million baby boomers, the largest age cohort. Which could lead to a higher growth CAGR going forward.

Source:USAFACTS

One thing I’ve yet to mention is covid, The pandemic led to a significant surge in total deaths, surpassing the typical trend growth and resulting in a substantial $4 billion increase in industry revenue. However, since 2021, there has been a normalization trend, with the total number of deaths decreasing from 3.46 million to 3.273 million in 2022. As of Q3 2023, the CDC data indicates a notable -12% decline in deaths for the year, suggesting that, if this trend continues, total deaths may return to 2019 levels by the end of 2023, marking the likely conclusion of normalization.Extrapolating total deaths from 2019 to 2023 using the average growth rate yields 3 million deaths, which is less than my extrapolation for this year. Carriage is much more conservative and estimates their funeral volumes will take one more year to get back to organic growth. Though the company noted revenue should begin to grow next year because of acquisitions.

Source: Carriage 2022 Annual Letter

Carriages main strategy for growth isn’t organic, it’s through acquisitions. Since its founding it’s been gobbling up the fragmented industry. Their acquisition strategy is to focus on larger businesses in growing markets. This can be seen as the number of funeral homes has declined since 2017 but total revenue has increased in that time. In general the goal is to grow 1-2% organically and 5-7% through acquisitions. With a target to get to 750M in Revenue by 2031. The company had a massive acquisition year in 2019 and as of Q3 2023 the company has done 41.7M in purchases.

Source: Author created chart, data from company 10-k’s

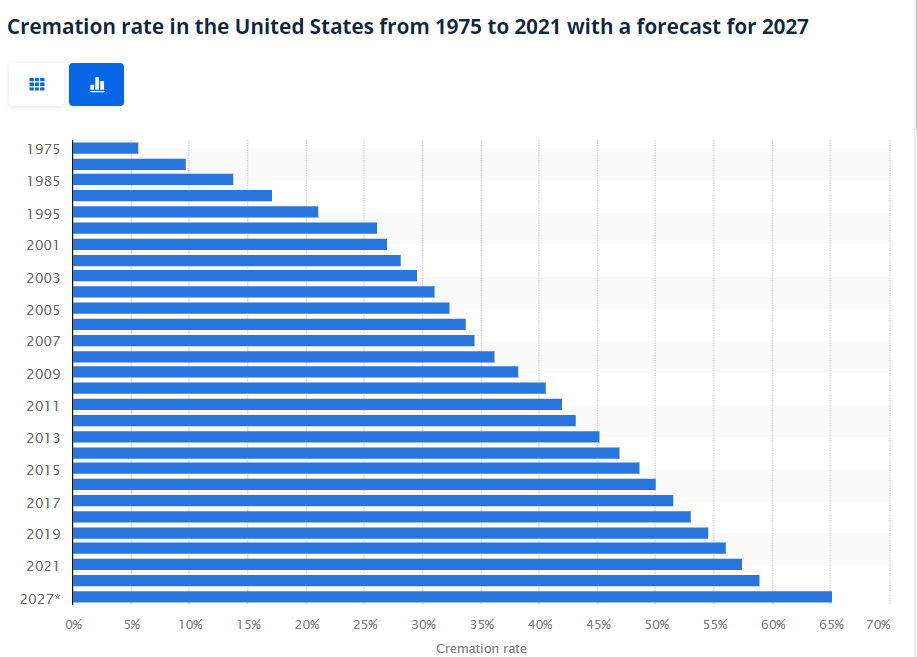

Another trend that’s been going on for awhile in the industry is the increasing use of cremations instead of traditional funerals where the whole body is left intact and is embalmed. This trend is due to cremations being a lot cheaper than the alternative on average by almost 50%. Cremations are a bit of a headwind for the company as they decrease the average price of a funeral which could decrease revenue. The company has been able to navigate through this by providing additional services “including video tributes, flowers, burial garments and memorial items such as urns, keepsake jewelry and other items“.

Source: Statista

History

Carriage was founded in 1991 and along with a number of other large companies was acquiring funeral homes at a rapid clip till 1999 when the death care bubble collapsed(never heard of this till researching this company). The big operators’ Carriage included had overpaid and over acquired funeral homes and till the late 2000s the industry was in restructuring mode as they sold off underperforming acquisitions and lowered debt. Compounded on this was a decline in deaths between 2001-2003. In these resturing years Carriage changed their operating model to a more decentralized structure which they still use today. Around 2007 Carriage began a new five year plan strategy which finally righted the ship and its been relatively smooth sailing since 2013.

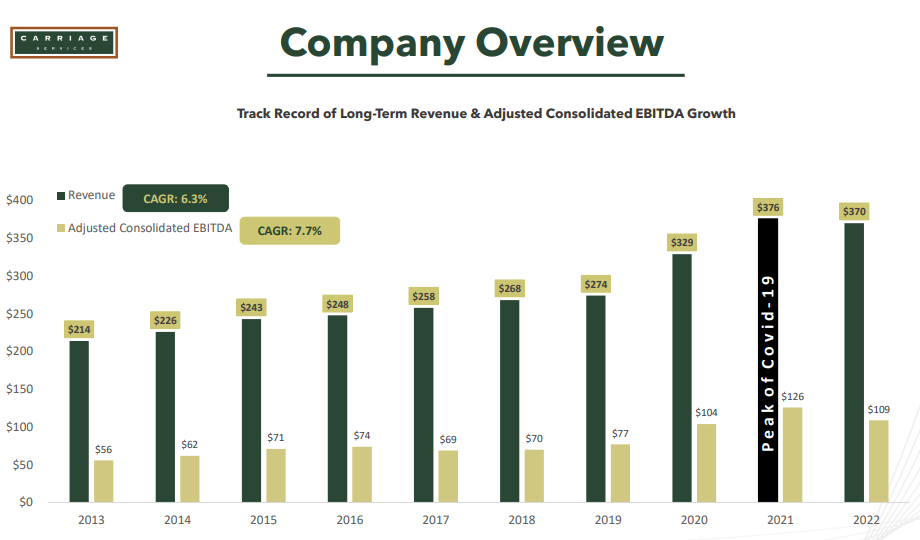

Since 2013 the company has grown revenue from $214M to $370M at a 6.3% CAGR.

Source: Q1 2023 Investor Presentation

The business doesn’t have very high returns on capital but due to the stability of the business Carraige is able to lever up to high levels to generate high return on equity. Average ROE using FCF instead of net income from 2013-2022 was 20%. The past three years of ROE has jumped to over 20% due to the company making large buybacks which lowered total equity and also the covid bump which increased FCF. If we exclude the past three years and look at 2013-2019 the ROE averaged 15% which is still good.

Source: Author Created Chart, Data from company 10-K

Overall the company is a decent business that grows stably and achieves decent rates of return with some leverage. Next I look at management.

Management

When I look at management I look for insider ownership, compensation structure, and capital allocation. Insiders own 12% of the stock with Melvin Payne one of the cofounders and current CEO owning 10.7% of the stock. This high percentage of insider ownership ensures alignment with shareholders. Melvin Payne though is 80 so there’s a question of who will lead after him. Carlos Quezada has been getting mentored for two years and will most likely be taking on the CEO job after Melvin. The company is also not opposed to being sold. Earlier this year Park Lawn(TSE:PLC) another publicly traded funeral operator was in talks to acquire Carriage. Park Lawn pulled out though which I attribute to the current interest rate environment. Also Carriage is a similar size to Park Lawn so it would have been a big acquisition to digest. Especially considering Park Lawn is actively talking about divesting properties. Carriage though could still be an acquisition target the two most likely targets would be Service Corp(SCI) which is the largest death care consolidator which is around 25 times larger than Carriage. Also Private Equity could make a bid as in 2022 Stonemor, a death care peer of Carriage was acquired by Axar Capital in 2022 at a 54% premium. I did not really look at management comp incentives too hard but overall it did not look that impressive.

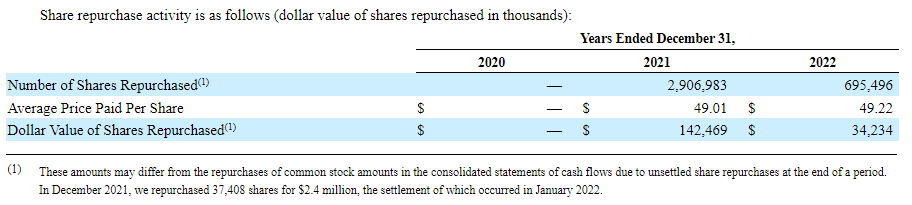

In terms of capital allocation Carriage seems to be good at acquisitions at least since 2013. The company has had a sustained increase in revenue and has averaged a decent ROE. In terms of buybacks the company has done less well. Since 2013 diluted shares outstanding has declined at a 4% CAGR. This is good however a lot of the buybacks were done recently at share prices a lot higher than now. For example the share price at the time of writing is $24 while buybacks in 2021 and 2022 were done at an average price of $49. Management in their 2022 annual letter did express regret on the share repurchases so maybe they’ll learn their lesson.

Source: 2022 Annual Report

Overall management seems kinda like a mixed bag. Lets see what customers think.

Google reviews

I find it valuable to assess the competence of management by examining Google reviews, as customer satisfaction is often indicative of a business’s future prospects. I looked at 18 locations or around 10% of the company’s properties. I literally just looked at the first 18 that appeared on the website with over 10 reviews. In total my sample averaged 4.83 stars with 1,135 reviews. Even though this is a limited sample, the consistently high customer ratings suggest that management might know what they’re doing.

| Name of Funeral Home | Location | Stars | Number of Ratings |

| A.A. Mariani & Son Funeral Home | 200 Hawkins Street, Providence, 02904 | 5.0 | 61 |

| Allison Funeral Service | 1101 North Travis Street, Liberty, 77575 | 5.0 | 20 |

| Alsip & Persons Funeral Chapel | 404 10th Avenue S, Nampa, 83651 | 4.9 | 127 |

| Angel Funeral Home | 2209 South Arthur Street, Amarillo, 79103 | 4.8 | 24 |

| Austin Funeral & Cremation Services | 807 Spokane Avenue, Whitefish, 59937 | 5.0 | 23 |

| Bagnasco & Calcaterra Funeral | 13650 15 Mile Road, Sterling Heights, 48312 | 4.9 | 74 |

| Bagnasco & Calcaterra Funeral Home | 25800 Harper Avenue, St Clair Shores, 48081 | 4.7 | 38 |

| Baker-Stevens-Parramore Funeral Home | 1500 Manchester Avenue, Middletown, 45042 | 4.6 | 16 |

| Baker-Stevens-Parramore Funeral Home | 6850 Roosevelt Avenue, Middletown, 45005 | 5.0 | 105 |

| Becker Ritter Funeral Home | 14075 W North Ave, Brookfield, WI 53005 | 4.9 | 18 |

| Berardinelli Family Funeral Service | 1399 Luisa Street, Santa Fe, 87505 | 4.9 | 130 |

| Bergin Funeral Home | 290 East Main Street, Waterbury, 06702 | 4.1 | 14 |

| Bradshaw-Carter Funeral Home & Cremations | 1734 West Alabama Street, Houston, 77098 | 4.9 | 145 |

| Bright Funeral Home | 405 S Main Street, Wake Forest, 27587 | 5.0 | 43 |

| Bryan & Hardwick Funeral Home | 2318 Maple Ave, Zanesville, OH 43701 | 5.0 | 70 |

| Bryant Funeral Home | 411 Old Town Road, Setauket- East Setauket, 11733 | 4.9 | 85 |

| Buck Ashcraft San Benito Funeral Home | 1400 77 BUS, San Benito, 78586 | 4.6 | 83 |

| Buckler-Johnston Funeral Home | 121 Main Street, Westerly, 02891 | 4.9 | 59 |

Valuation

Carriages share price has suffered over the past 3 years peaking in Dec 2021 at $64 and is now around $24 a share the same price as 2019. This is due to the failed merger with Park Lawn and the interest rate environment which is affecting profitability and the normalization of deaths from covid which is reducing funeral contract volumes. 2023 looks like the company will return to rev growth and FCF. But FCF is only growing because of working capital changes. I calculate cash flow earnings or CFE by adjusting FCF for working capital changes and subtracting it by depreciation instead of capex. Depreciation for Carriage is much more stable and overtime averages about the same. Using CFE, profitability will decline this year mostly due to increased interest rate charges which increased $9M as of Q3 2023. My estimate for CFE for 2023 is around $40-45 Million which will be a 2nd declining year as CFE peaked in 2021.

Carriage Financial Data

| Year | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 |

| REV | 375 | 370.17 | 375.89 | 329.45 | 274.07 | 267.99 | 258.14 | 248.20 | 242.50 | 226.12 | 213.07 |

| FCF | 50-60 | 34.94 | 59.36 | 67.72 | 27.84 | 35.47 | 28.83 | 33.24 | 20.20 | 20.47 | 29.15 |

| CFE | 40-45 | 54.02 | 67.22 | 51.13 | 35.16 | 30.96 | 35.25 | 37.01 | 35.32 | 34.22 | 31.60 |

| Funeral Contracts | 46,000 | 47,498 | 49,249 | 47,190 | 38,940 | 36,816 | 34,894 | 33,160 | 32,627 | 31,402 | 29,854 |

- CFE=OCF-ΔWorking Capital-Depreciation

- 2023 numbers are my projections

As I said above normalization from covid should be over and the company should begin growing at least inorganically in 2024 and organically in 2025. On top of that I don’t see interest rates going up much and actually as I said in my Bladex article i’m bearish rates. With Carriage gaining top line growth and interest rates being flat to declining the company should start to grow CFE again in 2024-2025 after peaking in 2021.

In terms of valuation I looked at the high and low market cap for the year for Carriage since 2013 then divided each by CFE for that year to get the high and low CFE multiples over time. On average Carriage has traded at 15 times CFE at its high for the year and 8.5 times CFE at its low for the year.

Carriage Historical CFE Multiple 2022-2013

| Year | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 |

| High | 1023.66 | 1211.58 | 578.28 | 513.14 | 532.11 | 513.03 | 508.26 | 475.41 | 410.42 | 499.81 |

| Low | 356.77 | 560.95 | 244.76 | 274.94 | 266.42 | 410.10 | 332.26 | 355.46 | 278.42 | 266.48 |

| P/CFE High | 10.33 | 15.23 | 23.70 | 16.45 | 16.57 | 15.09 | 13.86 | 14.39 | 13.89 | 12.99 |

| P/CFE Low | 5.18 | 5.31 | 10.97 | 6.96 | 8.88 | 7.56 | 11.08 | 9.41 | 10.39 | 8.81 |

- High: Highest market cap of the year

- Low: Lowest market cap of the year

At the current price, Carriage is quite attractive relative to history. If you use my estimate of CFE for the year the company is at 8-9 times CFE which is on the very low end of historical valuation.

Current Multiple Calculation

| Current Market Cap | $352M |

| 2023 CFE Estimate | $40-$45M |

| 2023 CFE Multiple | 8-9 |

Even looking at peers, Carriage is cheaper. Though the sector in general has been beaten up because of their shared trends, Carriage trades at 8.5 vs Service Corp at 11 and Park lawn at 11. Even if I adjust for leverage by looking at CFE before interest and taxes, Carriage is still in the cheaper bucket.

Peer Valuation

| Company | 2023 CFE Multiple | 2023 EV/CFE before Interest and Taxes |

| Carriage(CSV) | 8.5 | 16 |

| Park Lawn Corp(TSE:PLC) | 11 | 16 |

| Service Corporation(SCI) | 11 | 19 |

When estimating the expected return, I presume that the company can maintain a 15% Return on Equity (ROE) and at least a 6% growth rate, aligning with the company’s projections. This anticipated scenario would result in a payout ratio of 0.6, yielding a 7% shareholder yield at the current share price, and an overall expected return of approximately 13%. The payout is likely to be a combination of dividends and share repurchases. It’s important to note that this calculation does not incorporate any potential multiple expansion, which could further enhance the overall return. Considering Carriage’s current trading status at around 8.5 times CFE, and historical highs of 15 times CFE, there is potential for additional upside. However,the company could prioritize debt reduction, which would give a more conservative estimate of a 10% Internal Rate of Return (IRR) , which seems reasonable,this is a solid return for a stable business, excluding the impact of multiple expansion. Also I think Carriage could be an acquisition target from either Park Lawn, Service Corp or Private Equity which would juice returns even further and limit downside.

Risks

In terms of risks the main ones I see are interest rates, Acquisitions, future death rates and alternatives to traditional funerals.

Interest rates

Carriage is quite levered with a D/E ratio approaching 8 and a debt to ebitda ratio of 5.8. The higher for longer rates could dramatically decrease the company’s earnings going forward when the company refinances. The company has already been affected by higher rates as the company has a percentage of debt that is variable rate. Interest expense as of Q3 2023 is $9M higher compared to the prior year or 50%. However the majority of the company’s debt matures in 2029 so the company has time to weather the interest rate storm. Disclosure: I’m in the rates lower camp so I’m more comfortable with the leverage.

Acquisition indigestion

As with any roll up of an industry there is a risk that the buyer either overpays for companies or the acquired business does not perform as well as expected leading to indigestion in the companies stomach. Carriage focuses on tuck in acquisition which should limit this risk somewhat.

Future Death Rates

Cancer and heart disease are the number 1 and 2 killers in the United states. Any technological advancement that dramatically reduces these causes of death will have a negative impact on the business. Now if you hold this stock in a diversified portfolio the risk will be mitigated as your other positions will probably benefit from the increasing life spans and larger future population that those technologies will bring.

Alternatives

A traditional funeral with the whole body going into a grave is a relatively expensive endeavor costing between 5k to 10k. This has led to an increased amount of people using cremations instead of a traditional funeral as that costs significantly less. However there are even more alternatives such as a DIY cremation, becoming a coral reef, turning your deceased person into a diamond or art, donating your body to science, and shooting it into space. Alternatives to traditional burials could disrupt the company if Carriage cannot offer the service and also if its significantly cheaper than current options. I’m sure the future will bring even more options.

Conclusion

Carriage Services decent business currently trading at an appealing valuation, primarily attributed to prevailing headwinds. As these headwinds eventually dissipate, the outlook for Carriage Services appears promising and there is potential for decent returns going forward.

Top Four Metrics

The top four metrics are a couple of metrics that help me track a companies performance over time to help me evaluate whether I should continue to buy or sell out of a position.

For Carriage my four are

– CFE

– Funeral Contracts

– REV

– ROE

Disclosure

I added Carriage(CSV) to my portfolio in January.