Published 9/17/24

Vinci Partners 2024 Annual Review

It’s been over a year since I last wrote about Vinci Partners(VINP) and so It’s time for an annual review. For the most part most of Vinci financials have improved from the last time I wrote about them even after adjusting for the Real. AUM increased R$6B from 2022 to 2023 but has remained flat in 2024. AUM growth would have been better but Vinci’s IP&S segment hasn’t been doing great, down from R$26B in Q2 2023 to $25B in Q2 2024. With R$4B in net outflows. Though the IP&S segment is only 25% of revenue. Management expects AUM to increase as rates in Brazil continue down. Other segments such as Infrastructure, private equity and credit are doing much better.

| Year | Q2 2024 YTD | 2023 | 2022 | 2021 |

| AUM(In BRL) | 69 | 69 | 63 | 58 |

| FRE(In BRL) | 115M | 208M | 191M | 222M |

| FRE Margin | 49% | 46% | 47% | 48% |

| Cash Balance(In BRL) | 1.7B | 1.8B | 1.4B | 1.4B |

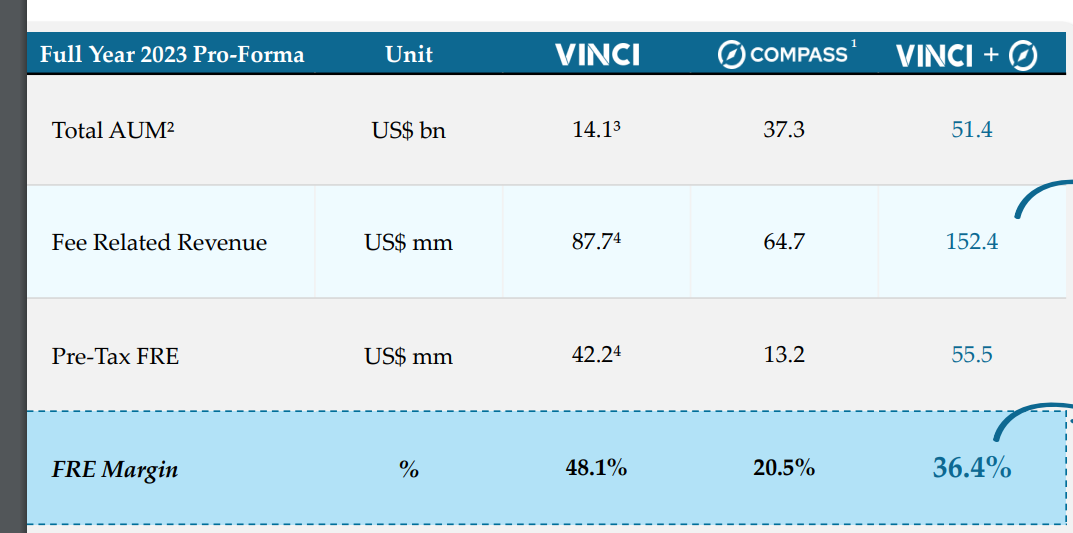

The biggest piece of news was Vinci acquisition of Compass which is another asset manager in LATAM mostly focused on IP&S or Investment products and solutions segment which allows clients to invest in everything from fixed income, foreign exchange currency, public equities, derivatives, and outside of Brazil. It also offers to do the client’s asset allocation and risk management. The acquisition will add $37B to Vinci’s AUM compared to Vinci’s $14.1B of AUM.

Most of that AUM is lower fee than Vinci AUM so even though Compass has doubled to AUM the company has less fee related revenue than Vinci and also much lower margins.

Source: Vinci and Compass 2024 Presentation

Looking at the price, I estimate that Vinci will pay around $160M, which is about a 15 times after tax FRE multiple which isn’t super expensive but not super cheap. Though alot of the purchase price is in stock and the transaction is yet to close so the price may be more or less depending on the stock price when the transaction closes in Q3 2024.

Even though Im not a big fan of the acquisition positives include

- Management has kept its stake about the same at 33% of the company since IPO

- AUM of higher fee segments have been growing at a decent pace and in general the company isn’t being hit as badly as other PE firms I’ve been looking at in the current not great fundraising environment

- Margins have been pretty stable

In terms of valuation Vinci is still quite cheap. With a market cap of $548M USD as of the time of writing. On the balance sheet net cash is about $220M and $40M in earnings with a 5.5 to 1 USD real. That would put Vinci at 8 times earnings which is quite cheap. I will continue to hold and add to Vinci going forward as performance as been decent and valuation is still cheap.