Published 12/11/2023

Pacific Smiles 2023 Review

I review each position in my portfolio on a yearly basis and now it’s time for Pacific Smiles Group(ASX:PSQ). In my previous article, I discussed Pacific Smiles as a recovery prospect post-COVID, striving to return to pre-pandemic performance levels in terms of both profitability and revenue per clinic. The year 2023 has shown improvement for the company, with nearly every key metric surpassing the figures from 2022. Despite this progress, challenges persist, notably in core profitability, which remains modest, and the high employee expense-to-revenue ratio.

Furthermore, the company is navigating a management transition following an activist event instigated by its founder. A more concerning development is the potential impact of a payroll tax issue. The government may demand that the company pay payroll tax on its fee-sharing contracts, posing a significant threat to profitability.

Key Metrics

For each position I decided to introduce 4 key metrics to track to assess the performance of the business. Which should make it easier for me to assess how every position is doing. For Pacific Smiles I picked Patient Fees per clinic, Clinics, OCF Margin, and CFE Margin. Patient fee per clinic was picked to assess the recovery from covid and the unit economics of the business. Clinics was picked as this is a growth story so I need to see unit growth. OCF margin and CFE margin are picked to assess profitability as the company struggled during covid.

All four metrics improved in 2023 pointing to a recovery. Profitability measured by CFE margin which I calculate as OCF-depreciation-changes in working capital. This clocked in at 2.25% in 2023 which is a far cry from the 7% in 2019 and closer to 10% before that.

Top 4 Metrics

| Year | 2023 | 2022 | 2021 | 2020 | 2019 |

| Patient Fees Per Clinic | 2080.77 | 1779.53 | 2211.01 | 1978.72 | 2101.12 |

| Clinics | 130 | 127 | 109 | 94 | 89 |

| OCF Margin | 16.56% | 4.38% | 14.93% | 9.90% | 17.21% |

| CFE Margin | 2.25% | -0.45% | 5.40% | 0.48% | 6.93% |

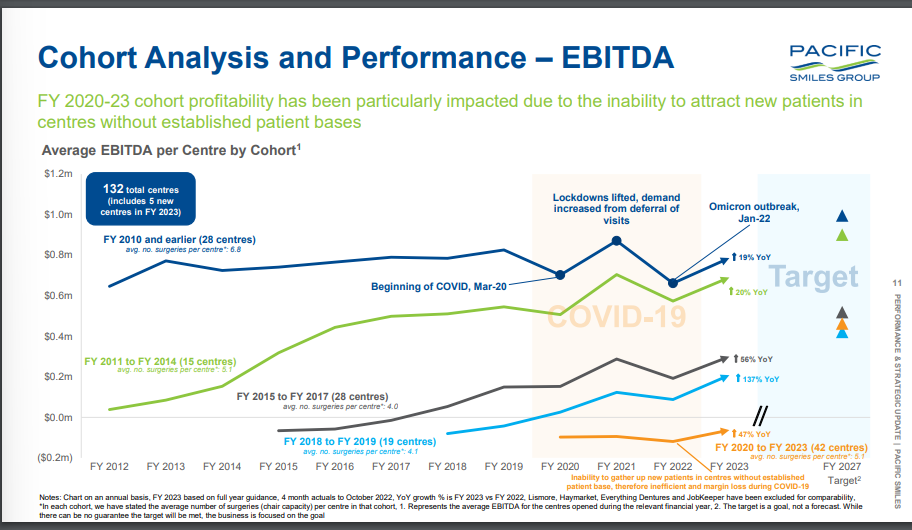

I attribute the low profitability to potential challenges with sales leverage and a potential excess of employees. Concerning sales leverage, the company generated 2.080 million in patient fees in 2023, slightly below the 2.101 million recorded in 2019. It typically takes three years for clinics to break even and five years to reach the target of 2.5 million in patient fees per clinic. Currently, the company has a significant number of clinics in the FY 2020 to FY 2023 cohort, which are relatively new and are impacting profitability negatively. This cohort is represented by the yellow line in the chart below.

Source: 2023 Pacific Smiles Performance Update

Management in their 2023 presentation points to the fact that covid disrupted the growth trajectory of the newer clinics which is possible. In the FY 2023 annual general meeting presentation YTD patient fees were up 10.5% YOY in FY 2024. Which lends credence to the fact that revenue is still recovering from covid.

Source: FY 2023 Pacific Smiles Presentation

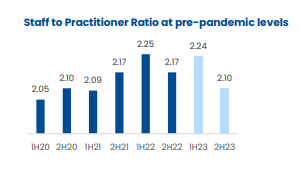

Another thing is the high employee expense to revenue ratio which is at 48% in 2023 compared to 42% in 2019. One reason for this is the high staff to practitioner ratio which measures the number of staff hours to dentist hours. This ratio was elevated in the covid years which implies a lot more hours of payroll being paid than normal. As of the end of 2023 this ratio has gone back to pre covid levels.

Source: FY 2023 Pacific Smiles Presentation

Another thing is the amount of employees which I can infer by the amount of dentists. In 2023 the company had around 900 dentists to 130 clinics vs 376 dentists to 80 clinics in 2018. The ratio of clinics to dentists in 2023 was 6.9 vs 4.7 in 2018. I don’t know why they have so many more dentists per clinic than they use too. Did they plan to grow faster than they did? Or are they planning to open a bunch of clinics in the next year? As of the 2023 presentation management has only announced 5 new clinic openings for 2024 which won’t put a dent in that ratio.

| Year | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 |

| Dentists/Clinics | 6.92 | 6.69 | 5.69 | 6.38 | 6.12 | 4.70 | 4.9 |

| Revenue/Dentists(In Thousands) | 183.69 | 164.08 | 247.06 | 200.09 | 224.14 | 278.00 | 266.68 |

Another item which is more for the future is that the state of New South Wales wants to impose a payroll tax on all revenue sharing contracts that Pacific does with their dentists. This would have a material impact on the company’s profitability. The company is currently challenging this decision. This action was prompted by a recent lawsuit in favor of the government pertaining to a similar contract Thomas and Naaz Pty Ltd v Chief Commissioner of State Revenue. This kinda sounds like Pacific may be liable. Pacific estimated a payment of 2 million would be owed. That amount would only be the state of New South Wales and would not include all the other states they operate in. Pacific Smiles says that this would flow through to patients but it may not be that simple.

With that said, next year should see increased profitability due to the high revenue growth. Also I’ll be emailing the company to ask why they got so many dentists. The payroll tax issue is an item that adds a lot of uncertainty about the future.

Management and Ownership Change

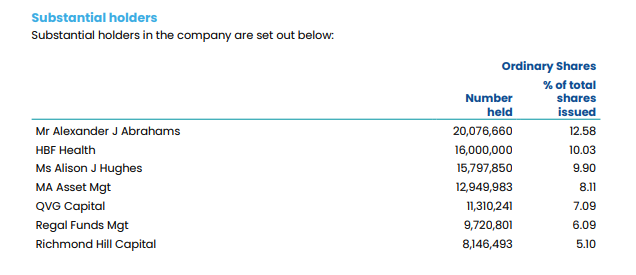

One of the founders Alexander Abrahams launched an unsuccessful activist campaign on his own company in Nov of 2022. Though he was pretty close to getting what he wanted and got two of his people elected onto the board. Most of the things voted on were tight, 40-50% For, to 40-50% Against. This might have been a factor as to why Phil Mckenzie the CEO of Pacific and a couple of directors have resigned this year. Phil Mckenize was brought in in 2018 when TDM Growth partners owned 16% of the shares. They have since sold out or at least a sold a majority of their position in the company as they no longer show up as a major shareholder in 2023. The founders Alexander Abrahams and Alison Hughes have also sold a lot of stock between 2019-2023 however they have not sold anything between the 2022 and 2023 annual reports. The fact that Abrahams has been selling stock for years and then all the sudden launched an activist campaign is kinda interesting.

In my last article I wrote how it was a good thing to have the founders with such large skin in the game. However since they have been selling down stock I don’t think I can really count them as strong insider owners that want the business to succeed.

No one in management really has a stake in the company and the management’s incentive scheme is not that great so in terms of strong management with aligned incentives I don’t really know if I can say the company has it. Unless Abrahams does another activist campaign and gets back on the board. Which could happen.

2023 Substantial Shareholders

Source: 2023 Annual Report

2019 Substantial Shareholders

Source: 2019 Annual Report

In other news Spheria Asset Management has been buying up lots of shares. In the month of November alone they have become a 5% stakeholder. They say they are a small cap value based fund. So we’ll see if they do anything.

Valuation

Since the company is currently suffering from low profitability I think EV/Sales is the best way to look at valuation. Currently the company is trading at 1.25 times EV/Sales. If you assume the company can get back to 10-12% EBIT margin then that would put the company at a 10-12 times EV/EBIT ratio which is pretty cheap. The EV/Sales is also cheaper than listed peers such as Q&M Dental which trades at 1.65 times EV/Sales and Dentalcorp which trades at over 2 times EV/Sales. Along the way the company will surely grow revenue so this multiple will be even lower. However due to the payroll tax item this valuation may not be as good as I think.

Conclusion

Overall the metrics are heading in the right direction. Though I don’t think management has good alignment with shareholders. Also there’s a good chance the company loses their challenge of the payroll tax item to the government which will have a large impact on profitability. Due to these two overhangs I think I won’t be adding to the company and may look to sell.

Look to Sell

- I’ll look to sell if profitability doesn’t consistently improve over the course of the next 3 years. Unless the company goes on a unit count growth spurt then I can give it more slack.

- If they lose the challenge to the government on the payroll tax item